Key Points:

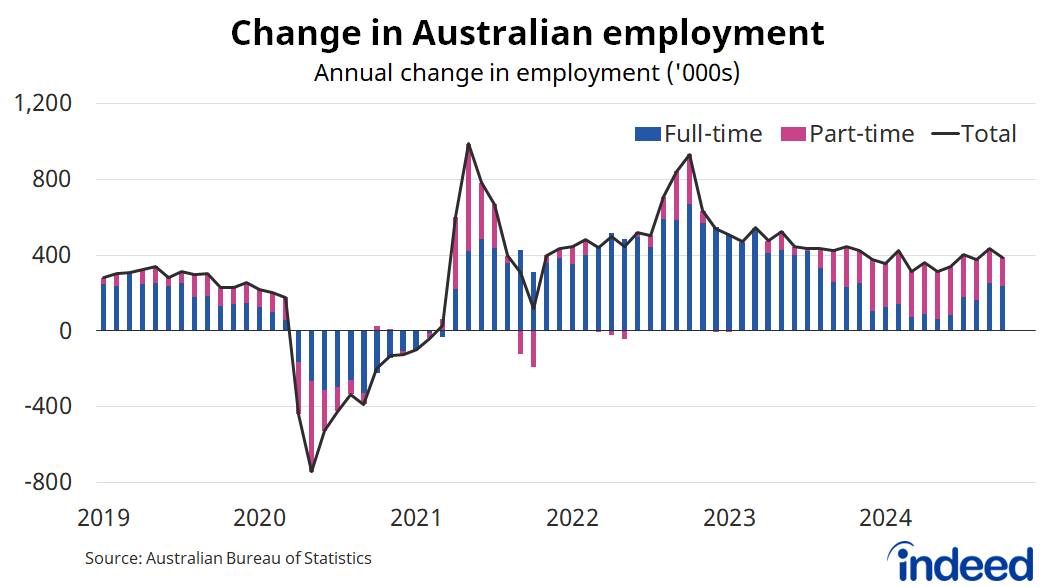

- Australian employment rose by 15,900 people in October, consolidating recent strong gains and bringing the total to around 387,000 over the past year.

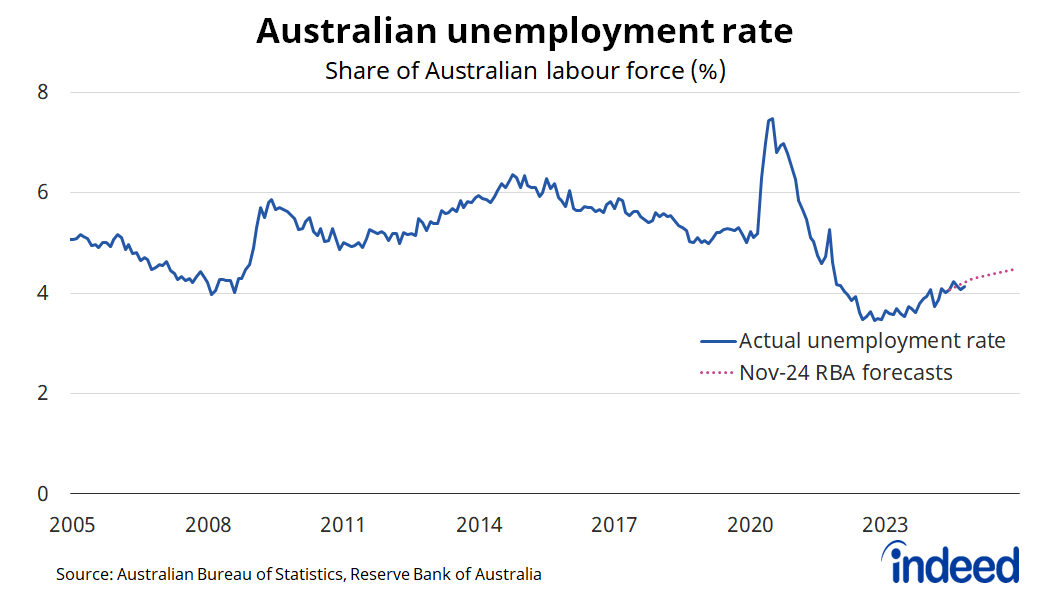

- Australia’s unemployment rate remained at 4.1% in October, with the underemployment rate dipping to its lowest since April last year.

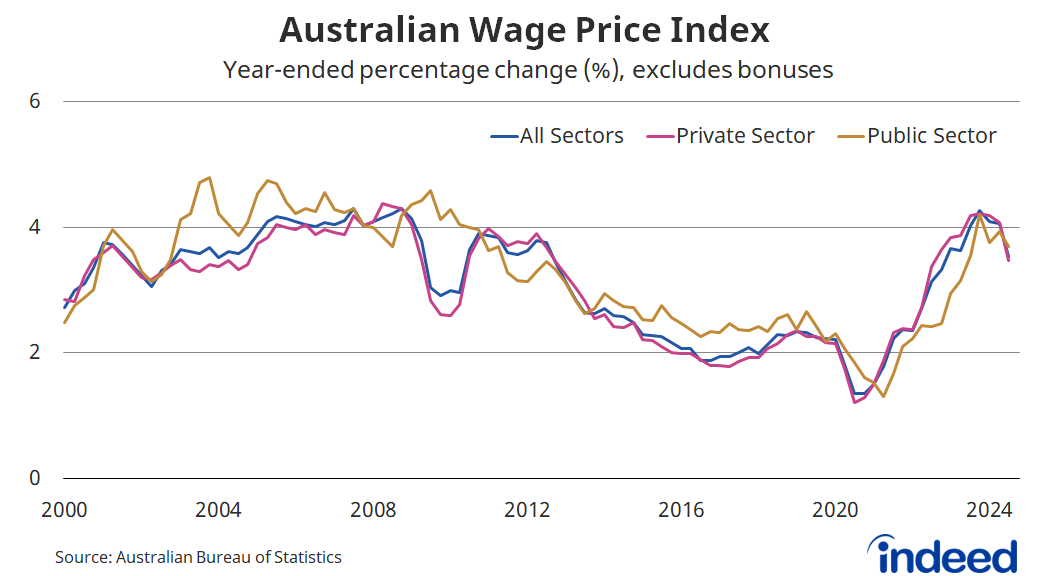

- Annual wage growth continues to ease, with public sector wage gains exceeding private sector gains for the first time since the March quarter 2021.

Australian employment rose 15,900 people in October — below market expectations — while the unemployment rate remained at 4.1%.

Australian employment continues to surge higher, driven by strong job creation across most sectors. Forward-looking indicators of labour demand — such as job vacancies and Indeed job postings — suggest that job creation in the near term will remain strong.

Australian employment has increased by around 387,000 people over the past year, including around 255,000 people over the past six months. That type of employment growth remains remarkable given the otherwise tepid economic environment.

Full-time employment accounts for over three-quarters of employment gains over the past six months. This indicates that the Australian economy continues to create high-quality, well-paying jobs.

Australia’s unemployment rate remained at 4.1% in October and is tracking broadly in line with the latest forecasts from the Reserve Bank of Australia. The rate of underemployment — which includes people who have a job but want more hours — dipped slightly in October to 6.2% and is now at its lowest level since April 2023.

Australia’s job market remains much tighter than it was pre-pandemic and is comparable to labour market conditions in the boom period prior to the global financial crisis.

Participation in the labour force dipped slightly from its record high in September but is up 0.3 percentage points over the past year. Participation continues to be supported by plenty of job opportunities and cost-of-living pressures.

Annual wage growth continues to ease

While quarterly wage growth remains solid, it is well past its peak, with quarterly gains the lowest in two-and-a-half years.

Both private and public sector wages rose by 0.8% in the September quarter, but for the first time since March 2021, annual growth in public sector wages exceeded that in the private sector. Public sector wages, and employment for that matter, tend to be less sensitive to market factors, often resulting in less volatility in wage growth from year to year.

Wage growth over the past year has been highest in the utilities sector (+5%), ahead of education & training (+4.4%) and administrative & support services (+3.9%). That wage gains remain strong in critical sectors, such as utilities, education and healthcare, points towards ongoing inflationary pressures across those key services.

Assessment and implications

Australia’s labour market remains incredibly tight and is proving highly resilient. The unemployment rate is low, employment growth is strong, and forward-looking measures of labour demand remain solid. This is a labour market at odds with Australia’s anemic economic performance.

Nothing in the latest labour force figures will shift the Reserve Bank of Australia’s thinking on monetary policy. And when combined with recent wage growth data, we have to conclude that Australia’s labour market dynamics simply aren’t consistent with cutting the cash rate anytime soon.