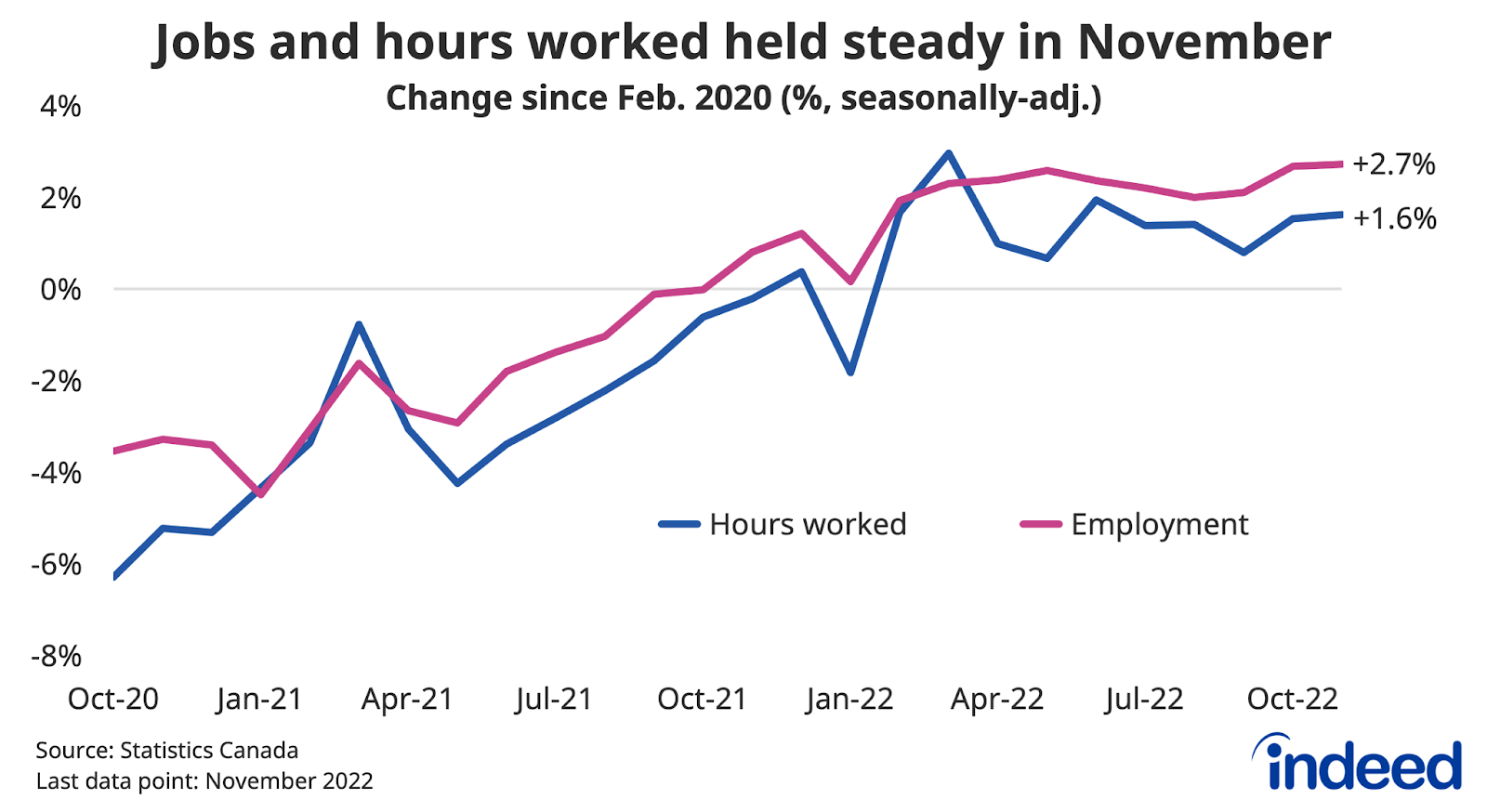

At this point in the economic cycle, instead of looking for labour market growth, we’re inspecting the job numbers for cracks in the armour. So far, conditions have steadied but remain resilient.

Overall employment and hours worked were fairly flat in November, while full-time jobs saw a decent rise, and layoff rates remained low. With the unemployment rate ticking down to 5.1%, near its multi-decade low, and uncertainty abound in the global economy, no news is good news.

The story was more mixed at the industry level. Construction gave back its October gains, while jobs in retail and wholesale trade have slipped since May. Both industries are potentially sensitive to the higher interest rate environment, which could weigh on their employment levels in the coming year.

With the unemployment rate already so low, the labour market’s strength is showing up in wage growth, rather than job growth. Average hourly earnings were up 5.6% year-over-year for a second straight month. Pay gains have been broad based, growth clocking in above 6% across accommodation and food service, professional service, construction, and manufacturing, among others.

Job postings on Indeed have held strong through November, suggesting labour demand – and by extension – wage gains could maintain a solid pace. However, whether this actually boosts household purchasing power depends on inflation falling back. Achieving the latter is the Bank of Canada’s goal, but in the process, the tightening cycle both at home and abroad, could also dislodge the current job seekers’ market.