Key Points:

- Job postings remain high and the labour market very tight despite gloomy economic outlook.

- Tech hiring has cooled in recent months.

- Employment regains some lost ground and inactivity falls, but real wages are compressed further.

- Redundancy notifications remain low, suggesting no plans for widespread layoffs.

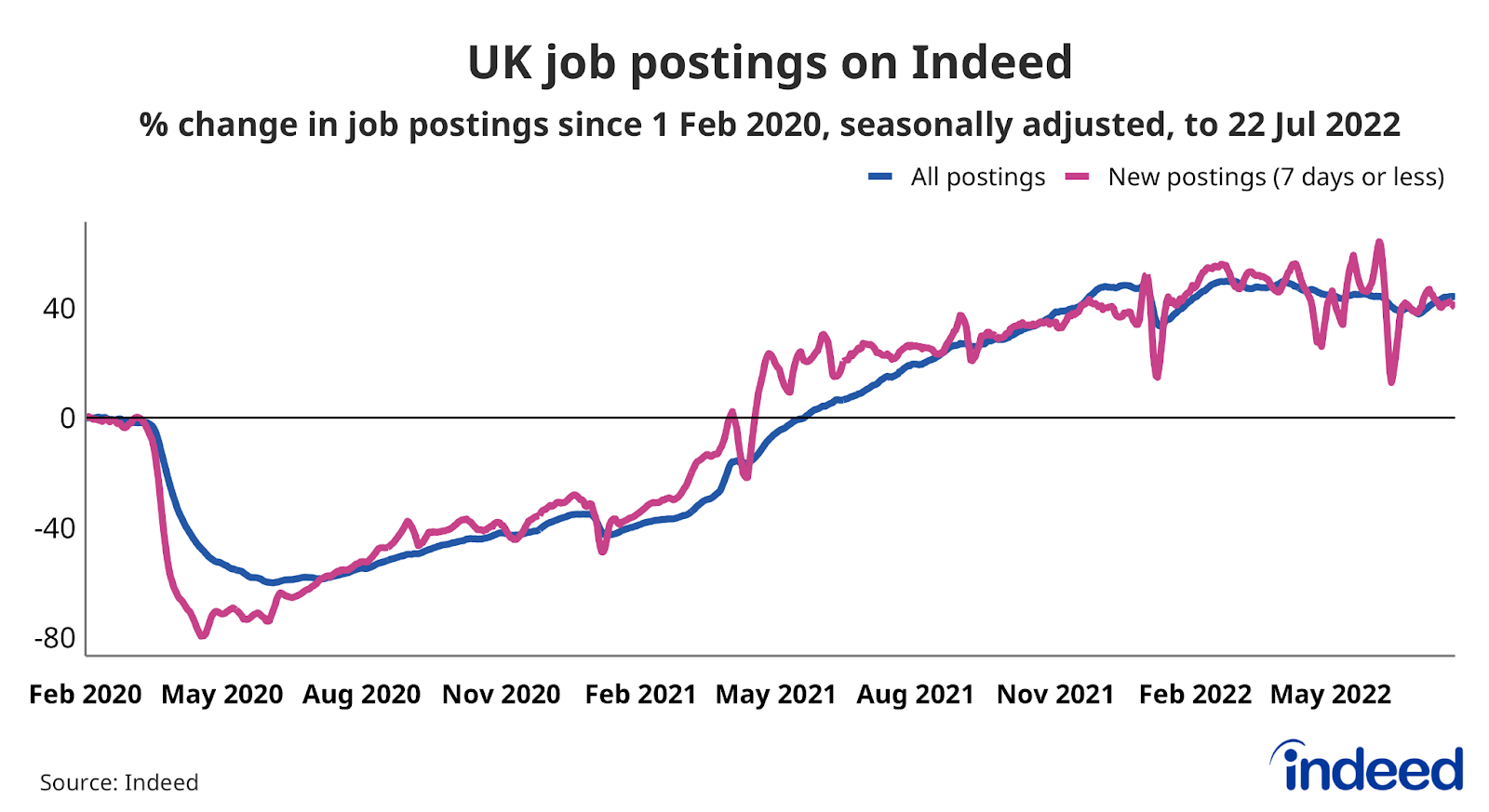

Job postings remain elevated

Real-time data from Indeed job postings continue to indicate strong demand for staff. Postings were 44% above the 1 February 2020, pre-pandemic baseline, seasonally adjusted, as of 22 July 2022. Though down from a post-pandemic high of 50% on 31 March, the trend has remained stable in recent months despite bleak forecasts for the UK economy. Many employers continue to face staffing gaps amid a tight labour market. But it’s not a case of ‘stale’ vacancies; the inflow of new job postings remains high.

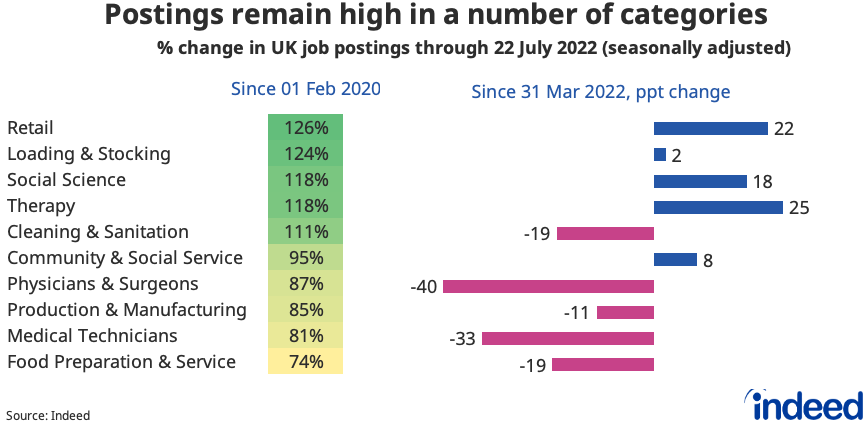

Job postings remain elevated in a number of categories, with softening in some offset by growth in others. Five categories — retail, loading & stocking, social science, therapy and cleaning & sanitation — have at least doubled since the onset of the pandemic, with four of those posting further gains since the end of the first quarter.

But most categories have seen a correction recently. Since 31 March 2022, 36 out of the 49 occupational categories we publish on Github saw declines. Broadly speaking, we can observe five groups in terms of recent job posting trends.

First, we have pandemic winners still growing or stable, including retail, loading & stocking and therapy. Second are pandemic winners experiencing a correction or normalisation, including several healthcare categories, food service, cleaning, manufacturing and tech. Third, we have stable active hirers, including care, driving and finance. Fourth, pandemic laggards still catching up as hiring remains challenging, including nursing, legal and childcare. Fifth, pandemic laggards slumping back, of which only beauty & wellness fits the bill.

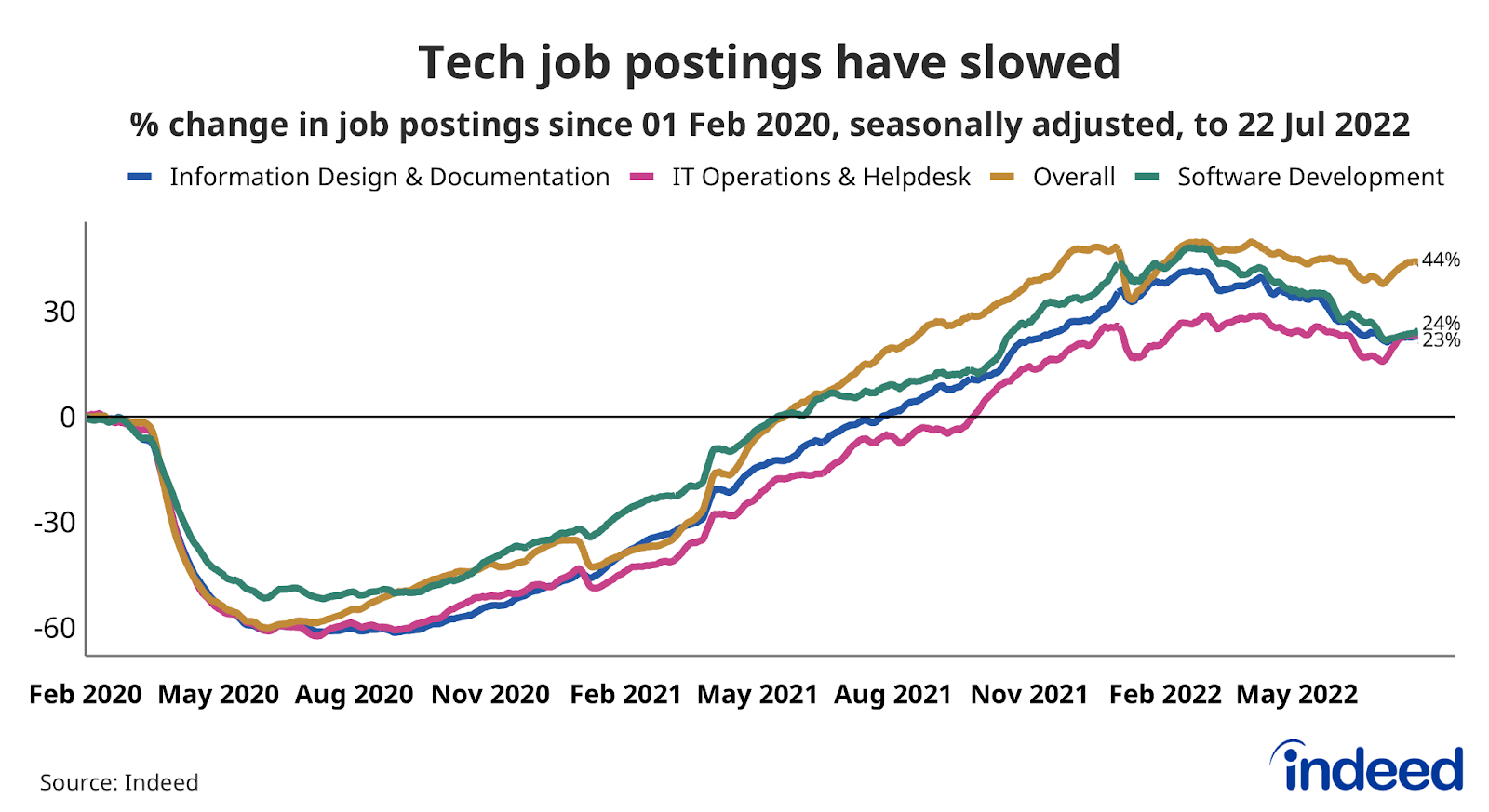

Tech hiring slowdown

Tech is one area where job postings have slowed, mirroring trends in the US. The software development category (which includes titles such as software engineer, developer and product manager) peaked in February at 48% above the pre-pandemic baseline, but has now slipped to 24%. IT operations & helpdesk (which includes IT support, network engineers and data administrators) and information design & documentation (which includes business analysts, IT security specialists and user experience designers) have also cooled.

Labour Market Overview

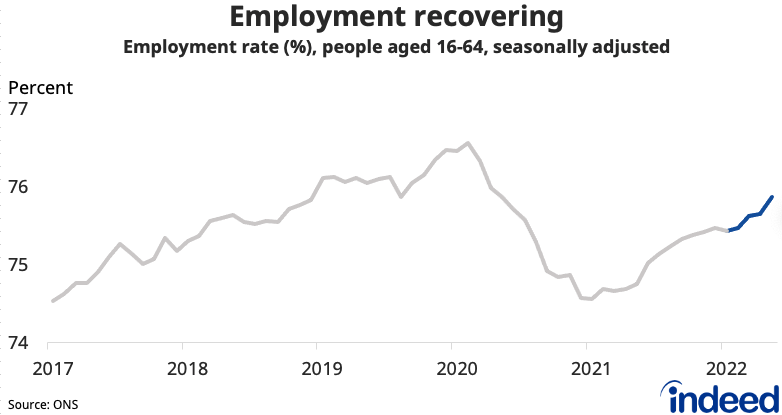

The latest Office for National Statistics (ONS) data contained mixed news. On the positive side, employment continued to recover ground. The employment rate among working age people climbed to 75.9% in the three months to May, up from its pandemic low of 74.6% but remaining below its early 2020 peak of 76.6%. The number of people in employment remains 210,000 below its pre-pandemic level.

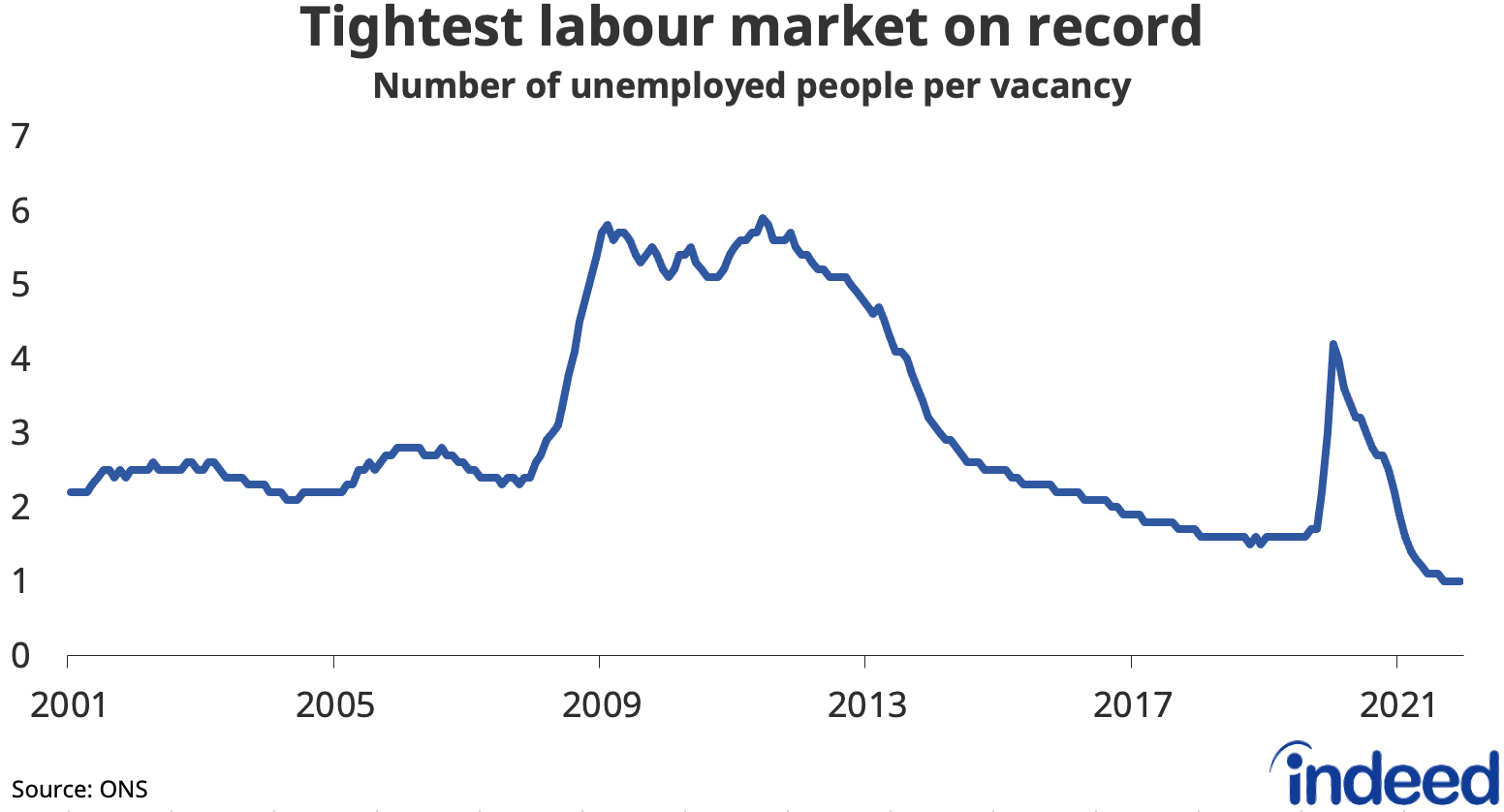

Vacancies remained high at just under 1.3 million in the three months to June, though have plateaued in the latest quarter. With unemployment remaining low at 3.8%, there continues to be less than one unemployed jobseeker per vacancy — the tightest labour market in decades.

Positive trend in labour market participation

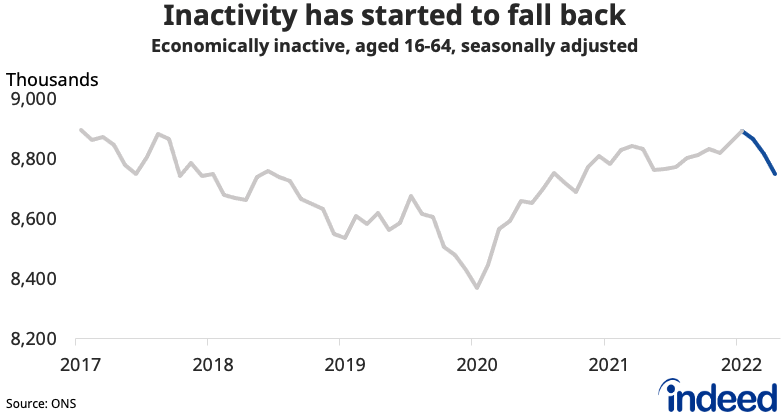

There was also positive news on labour market participation. Economic inactivity among working age people fell further in the three months to May and is down by 144,000 from January’s peak. However, it remains some 378,000 higher than on the eve of the pandemic. The UK is an international outlier in terms of the scale and duration of higher inactivity since the pandemic, with an increase in long-term sickness a key driver.

Over two-thirds of that rise in inactivity has been among people aged 50-64. However, there are signs that some older workers are starting to return to the labour force. The inactivity rate among people aged 50-64 has fallen from 27.2% to 26.8% between February and May. That said, it remains well below the 25.2% rate in February 2020 prior to the pandemic.

In the US, there has been a trend of ‘unretirements’ and something similar may be emerging in the UK. Some people who took early retirement may be reconsidering amid cost of living pressures eating into savings and falling investment values hitting pension pots.

Wages continue to be squeezed by inflation

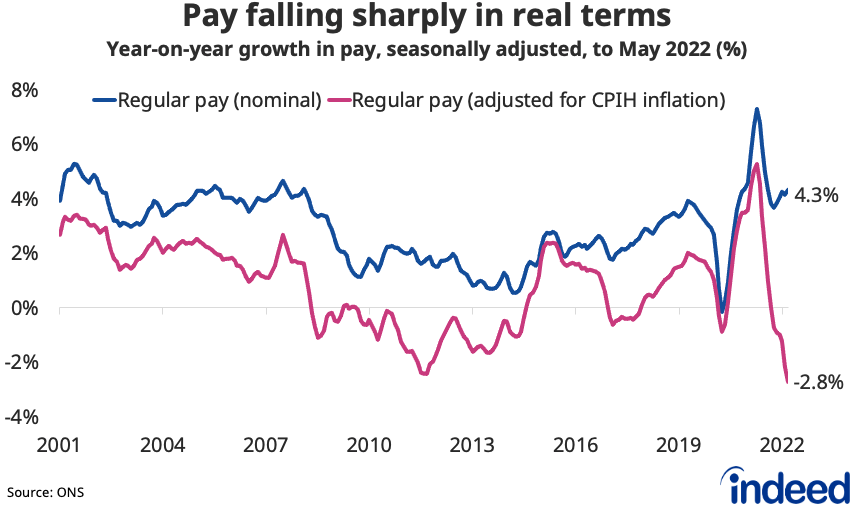

Meanwhile, real wages continue to be squeezed by high inflation. Despite regular pay growth running at a historically strong rate of 4.3% year over year (y/y) in the three months to May, real pay was down 2.8% y/y. That’s the sharpest fall on comparable data back to 2001.

Outlook

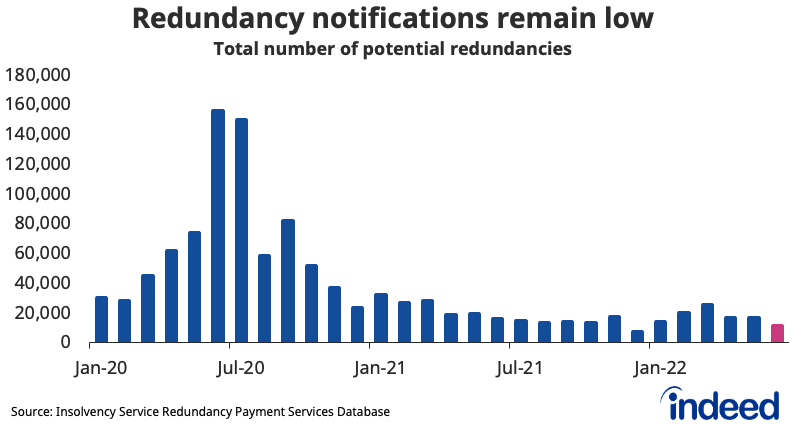

For now, the UK labour market is holding up. Real-time indicators like job postings continue to show robust demand for staff. Another early labour market indicator is redundancy notifications, but these remain low and certainly don’t suggest widespread plans to cut staff at present.

The Bank of England is treading a fine line on calibrating monetary policy tightening, as it bids to cool inflationary pressures (including factoring in fiscal policies depending on the outcome of the Prime Ministerial race). From a labour market perspective, the benign scenario is a gradual softening in vacancies accompanied by a further pick-up in labour supply. That would ease chronic hiring challenges and cool wage pressures.

A less benign economic scenario could involve a sharp slowdown in consumer spending and rising job losses, which policymakers will clearly be keen to avoid, though aren’t being helped by developments in global energy markets which point to further cost of living pain over the winter.

But while financial pressures may draw more people back into the workforce, high rates of long-term sickness and reduced access to cheaper EU labour post-Brexit suggest tight market conditions are not going to go away any time soon.

We host the underlying job-postings chart data on Github as downloadable CSV files. Typically, it will be updated with the latest data one day after this blog post was published.

Methodology

All figures in this blogpost are the percentage change in seasonally-adjusted job postings since 1 February, 2020, using a seven-day trailing average. 1 February, 2020, is our pre-pandemic baseline. We seasonally adjust each series based on historical patterns in 2017, 2018, and 2019. Each series, including the national trend, occupational sectors, and sub-national geographies, is seasonally adjusted separately. We adopted this methodology in January 2021.

The number of job postings on Indeed.com, whether related to paid or unpaid job solicitations, is not indicative of potential revenue or earnings of Indeed, which comprises a significant percentage of the HR Technology segment of its parent company, Recruit Holdings Co., Ltd. Job posting numbers are provided for information purposes only and should not be viewed as an indicator of performance of Indeed or Recruit. Please refer to the Recruit Holdings investor relations website and regulatory filings in Japan for more detailed information on revenue generation by Recruit’s HR Technology segment.