Key Points:

- The labour market continues to soften, though it’s still somewhat tight with 1.6 unemployed persons per vacancy.

- Wage growth remains high and its evolution will be a key factor in the timing of any interest rate cuts.

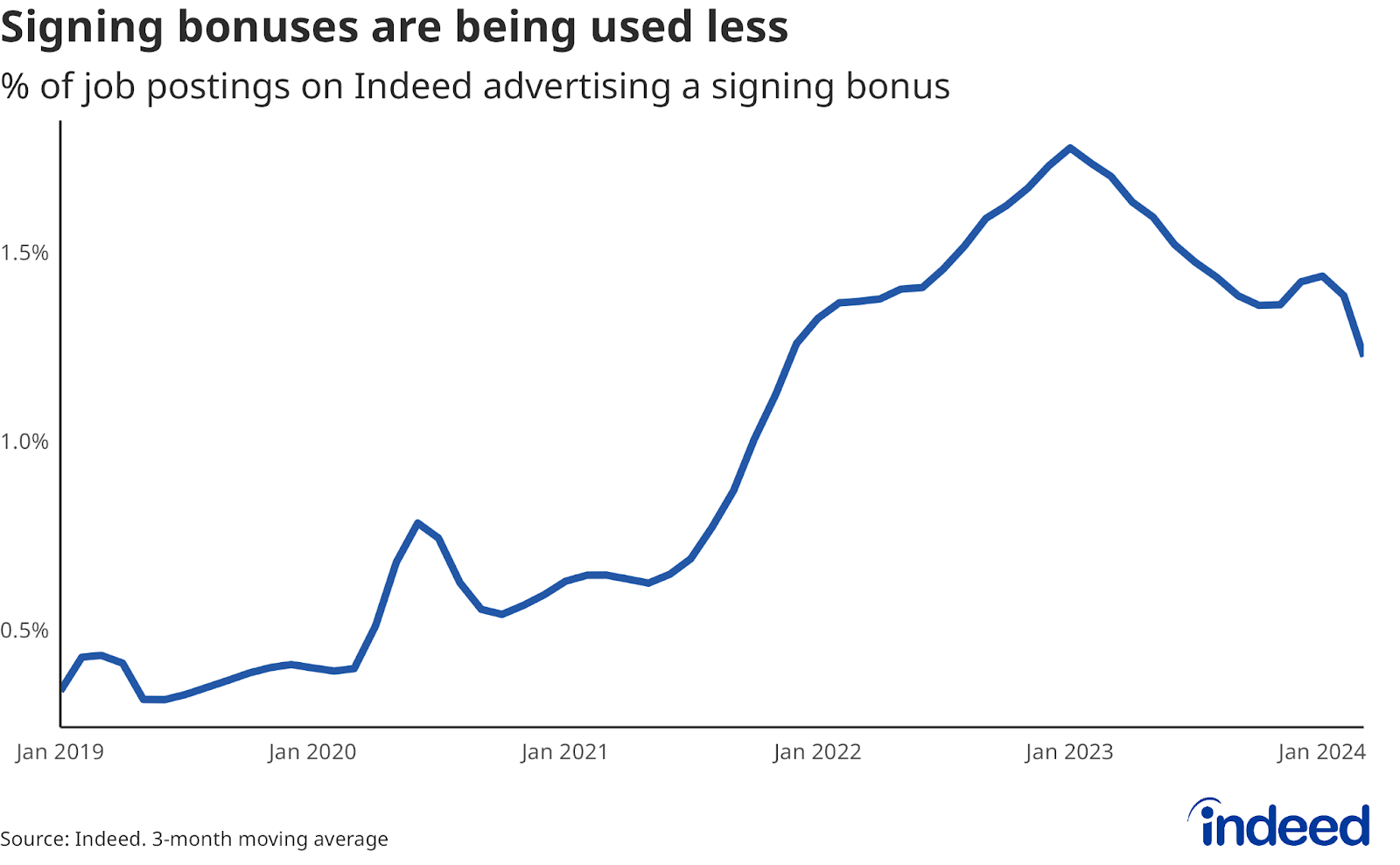

- Signing bonuses are being used less frequently than before, with the share of postings offering them having dropped from 1.8% to 1.3%.

The UK labour market has cooled markedly, but is still generating robust wage growth. While good news for workers who are seeing their pay outpace inflation, wage growth persistence could mean interest rates staying high for longer.

Spotlight: Signing bonuses are being used less

At the peak of post-pandemic staff shortages, we saw more employers offering financial incentives such as one-off joining bonuses to try and entice workers. The share of job postings offering a signing bonus peaked at 1.8% in January 2023. Their use has diminished, with the share dropping to 1.3% as of March 2024. That’s a sign of employers recruiting with less intensity as the labour market has cooled, though the prevalence of signing bonuses remains more than double the 2019 level. The trend in signing bonuses echoes that of posted wage growth, which has eased from peaks but is still running high.

Labour Market Overview

The labour market continues to gradually cool but continued high wage growth underlines concerns over inflation persistence. The latest Office for National Statistics (ONS) figures showed a larger than expected rise in unemployment to 4.2% in the three months to February, alongside a drop in employment. Inactivity also rose further and remains well above pre-pandemic levels. That said, there remains a caveat over the provenance of these figures given underlying data quality concerns, with the ONS advising caution in interpreting changes.

Unemployment remains low but is up from 3.8% at the end of 2023. Vacancies fell on the quarter to 916,000 and are well down from peaks, albeit still 12% above their level on the eve of the pandemic. The ratio of unemployed people to vacancies now stands at 1.6, still somewhat tight relative to trends seen over the last 20 years but up from a low of 1.0 seen in 2022.

Despite having cooled, the labour market is still generating strong wage growth at 6.0% year-on-year in regular pay in the three months to February. Short-term momentum is a bit softer than that, with the annual comparison still being influenced by chunky pay awards from last spring which will fall out of the calculation in coming months. On the other hand, a near-10% uplift in the minimum wage came into effect on 1 April and will feed into the figures.

Indeed data shows advertised wages for new hires continuing to grow at a strong pace of 6.2% year-on-year in March, suggesting that momentum in pay growth is likely to continue in the near term.

Conclusion

With a general election looming, all eyes are on when the Bank of England might start cutting interest rates and ease the burden on households. The challenge for the Bank is that though inflation is down and the labour market weakening, its ducks aren’t yet all in a row for an easing. Some indicators suggest a risk that keeping inflation down at the 2% target over the medium term could still be tricky. The persistence of wage growth will be one key determinant of that, alongside services inflation.

In the US, expectations of rate cuts this year have diminished recently following stubborn inflation prints. Bank of England Governor Bailey has noted that inflation dynamics in the UK differ from those in the US (due to greater weakness on the demand side of the economy), meaning the Bank might cut rates before the Federal Reserve does.

But the UK arguably faces greater constraints than the US on the supply side of the economy, notably the labour market. One sign of that is posted wage growth, which in the UK is running at double the rate seen in the US. These concerns underpin the case of hawks on the Bank’s Monetary Policy Committee for keeping rates higher for longer. The doves’ case is that rising unemployment and easing staff shortages will erode workers’ bargaining power, leading to easing pay growth. Economic data over the next two to three months will give a clearer steer on what comes next. On the positive side, data does suggest the UK pulled out of recession in the first quarter.

Wage dynamics also remain important for employers in keeping their reward strategies aligned to the market. The most up-to-date data on wage growth, along with job postings and remote/hybrid trends, is available on our newly launched Hiring Lab Data Portal.

Hiring Lab Data

Job postings data is available on our Data Portal. We also host the underlying job-postings chart data on Github as downloadable CSV files. Typically, it will be updated with the latest data one day after this blog post was published.

Methodology

Data on seasonally adjusted Indeed job postings are an index of the number of seasonally adjusted job postings on a given day, using a seven-day trailing average. Feb. 1, 2020, is our pre-pandemic baseline, so the index is set to 100 on that day. We seasonally adjust each series based on historical patterns in 2017, 2018, and 2019. We adopted this methodology in January 2021. Data for several dates in 2021 and 2022 are missing and were interpolated. Non-seasonally adjusted data are calculated in a similar manner, except that the data are not adjusted to historical patterns.

To calculate the average rate of wage growth, we follow an approach similar to the Atlanta Fed US Wage Growth Tracker, but we track jobs, not individuals. We begin by calculating the median posted wage for each country, month, job title, region and salary type (hourly, monthly or annual). Within each country, we then calculate year-on-year wage growth for each job title-region-salary type combination, generating a monthly distribution. Our monthly measure of wage growth for the country is the median of that distribution.

The number of job postings on Indeed.com, whether related to paid or unpaid job solicitations, is not indicative of potential revenue or earnings of Indeed, which comprises a significant percentage of the HR Technology segment of its parent company, Recruit Holdings Co., Ltd. Job posting numbers are provided for information purposes only and should not be viewed as an indicator of performance of Indeed or Recruit. Please refer to the Recruit Holdings investor relations website and regulatory filings in Japan for more detailed information on revenue generation by Recruit’s HR Technology segment.