Key Points:

- The UK economy outperformed low expectations in 2024 but has slowed in recent months, with concerns over the labour market’s outlook.

- Headwinds to hiring have mounted as a result of the Budget’s policy changes, though a handful of sectors could see a boost from government spending plans.

- Job postings have seen a sustained and broad-based slowdown this year, with almost all categories having seen falls.

- Waning usage of signing bonuses and an increased prevalence of zero-hours contracts are signs that employers may be gaining more bargaining power.

- Posted wage growth has eased but remains strong, particularly for lower-paid and in-person roles, but is likely to gradually wane heading into next year.

- Remote/hybrid flexibility in postings has dipped from peaks but persists at a much higher level than pre-pandemic.

- GenAI tools are not yet widely adopted, but are gaining traction in a handful of sectors.

The UK economy performed a little better than expected this year, but sails toward 2025 in choppy waters. While the first half of this year saw a solid recovery from the shallow technical recession seen in late-2023, the economy’s motors have been stalling in recent months and there are particular concerns about the labour market’s prospects.

On the positive side, GDP projections for this year and next have been upgraded by many forecasters, with growth set to quicken in 2025. The International Monetary Fund raised its 2024 UK growth forecast from 0.4% to 1.1%, and said it expects 1.5% growth in 2025, placing the UK near the middle of the pack among advanced economies. The Office for Budget Responsibility and Bank of England are both slightly more optimistic, each forecasting roughly 2% GDP growth next year.

Less positively, this doesn’t look likely to translate into a hiring upswing, with government policy changes presenting multiple headwinds. The combination of a hike in employer National Insurance contributions and lowering of their threshold, higher minimum wages, increased business rates and a new workers’ rights package have been widely met by warnings of a hit to employment and wages. Sectors that typically employ large numbers of lower-paid workers, including retail and hospitality, are likely to be most impacted by these changes, though the effects will be felt broadly across the labour market.

At the higher-paid end, knowledge-work occupations have experienced a marked slowdown in hiring over the past couple of years amid a so-called ‘white collar recession.’ With business confidence remaining subdued amid still-restrictive monetary policy and ongoing global uncertainty, caution is likely to remain the watchword for many employers.

The overall stance of the Budget was a fiscal expansion, with higher public spending financed by increased borrowing and tax rises. That’s set to boost growth in the short-term, though not expected to deliver a sustained upshift beyond the first couple of years. Higher government spending implies that monetary policy will have to be kept tighter than it otherwise might be to keep inflation down.

The Bank of England has cut interest rates twice in recent months but is not yet ready to declare victory over inflation. Alongside the Budget impact, the Bank remains mindful of stubborn services inflation and wage growth, signalling that further rate reductions are likely to be gradual.

Waters muddied by faulty labour market data

A major challenge for policymakers is that it’s very difficult to get a clean read on the state of the UK labour market due to data quality issues. The response rate to the Office for National Statistics’ (ONS) flagship Labour Force Survey (LFS) remains so low that several key statistical measures, including employment, unemployment and inactivity, continue to be unreliable.

But taken at face value, the figures indicate that the UK employment rate has not yet recovered to pre-pandemic levels, unlike other leading advanced economies. That’s been accompanied by a modest rise in unemployment and a large increase in the number of inactive workers, driven in particular by rising long-term sickness.

However, alternative estimates of employment, based on administrative data and updated population figures not accounted for in the ONS statistics, suggest much stronger jobs growth since the pandemic. If that’s true, it would imply some combination of lower unemployment and/or lower inactivity (researchers suggest inactivity could be substantially lower than suggested by the ONS figures). Regardless of these uncertainties, the Labour government has made boosting labour force participation a priority to help unlock economic growth.

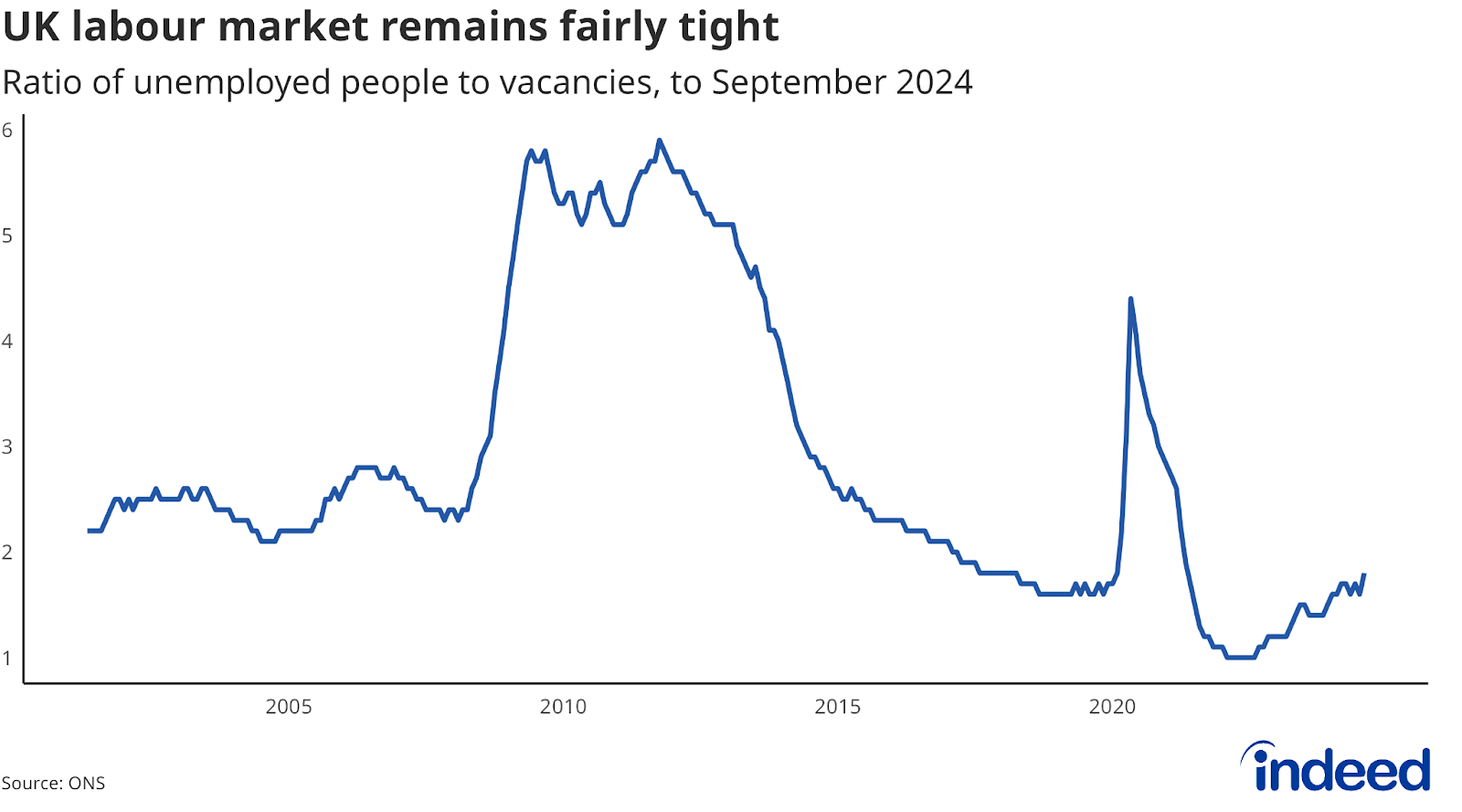

What is clear is that the UK labour market has cooled substantially from post-pandemic highs. Vacancies are well down from the heady peaks of 2022 (the official vacancy statistics are not affected by the LFS issues). But even after this prolonged slowdown, it remains a fairly tight market by the standards of the past two decades. The ratio of unemployed people for each vacancy has risen to 1.8, from 1 back in 2022, but remains well below longer-term, pre-pandemic averages of around 3.

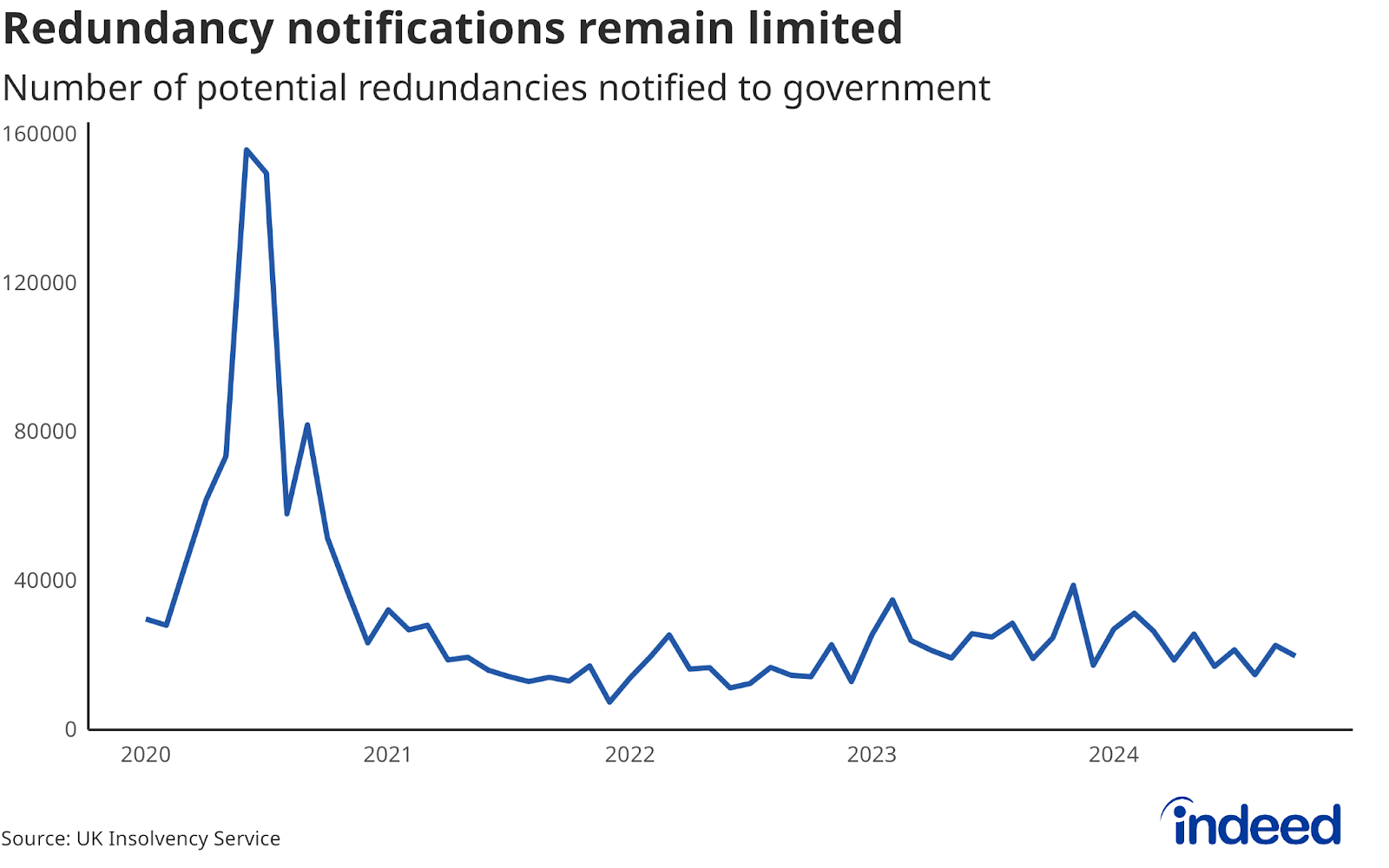

Relatively subdued layoff activity has also helped keep a lid on unemployment. But that could change if the economy performs weaker than expected and as employers continue to weigh the impact of the Budget on their workforce plans. A sustained upshift in redundancy notifications beyond their recent range of 20,000-40,000 per month could presage a rise in the unemployment rate towards 5% and materially weigh on economic growth next year.

The election of Donald Trump as US president is a key unknown for the UK economy. UK growth could be cut in half if he enacts significant trade tariffs, according to analysis from the National Institute of Economic and Social Research. Those tariffs would hit export-oriented sectors in particular, but would be felt across the broader economy. Conversely, some have speculated that the incoming US administration might be sympathetic to a preferential trade deal with the UK. Geopolitics, in general, also remains an ever-present risk to the outlook, including the possibility of escalating regional conflicts and/or a renewed spike in global energy prices.

Job postings have fallen in almost all occupational categories in 2024

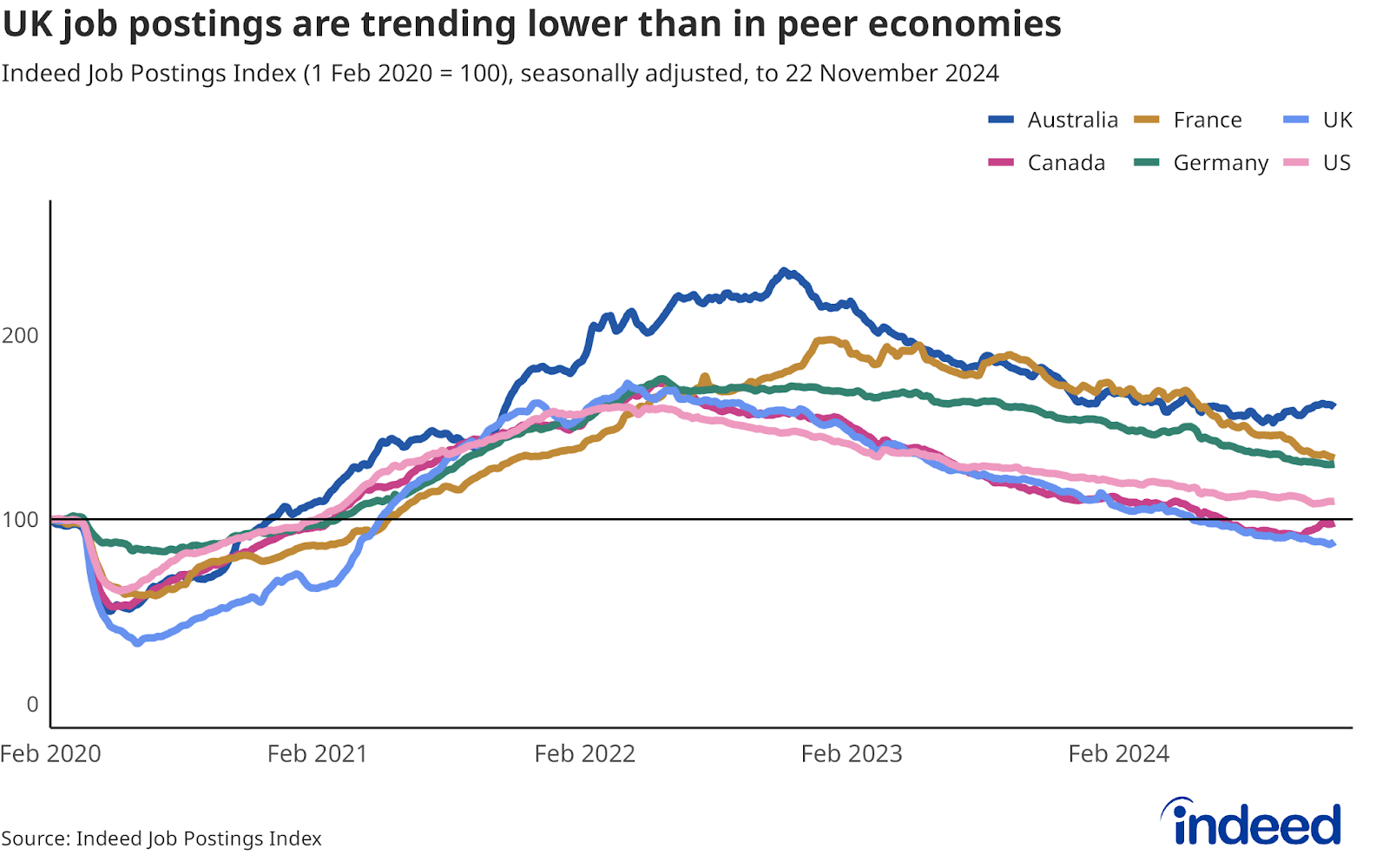

After peaking in early 2022, UK job postings have spent the past two-and-a-half years beating a slow retreat. As of 22 November, UK job postings on Indeed were 12% below their pre-pandemic baseline, down from a peak of 74% above the baseline back in March 2022. The overall level of UK postings is weaker than in peer countries, including Australia, Canada, France, Germany and the US (total job postings remain above pre-pandemic levels in all of those nations except Canada). The 23.7% decline in UK postings over the past year is also the largest such decline among those countries.

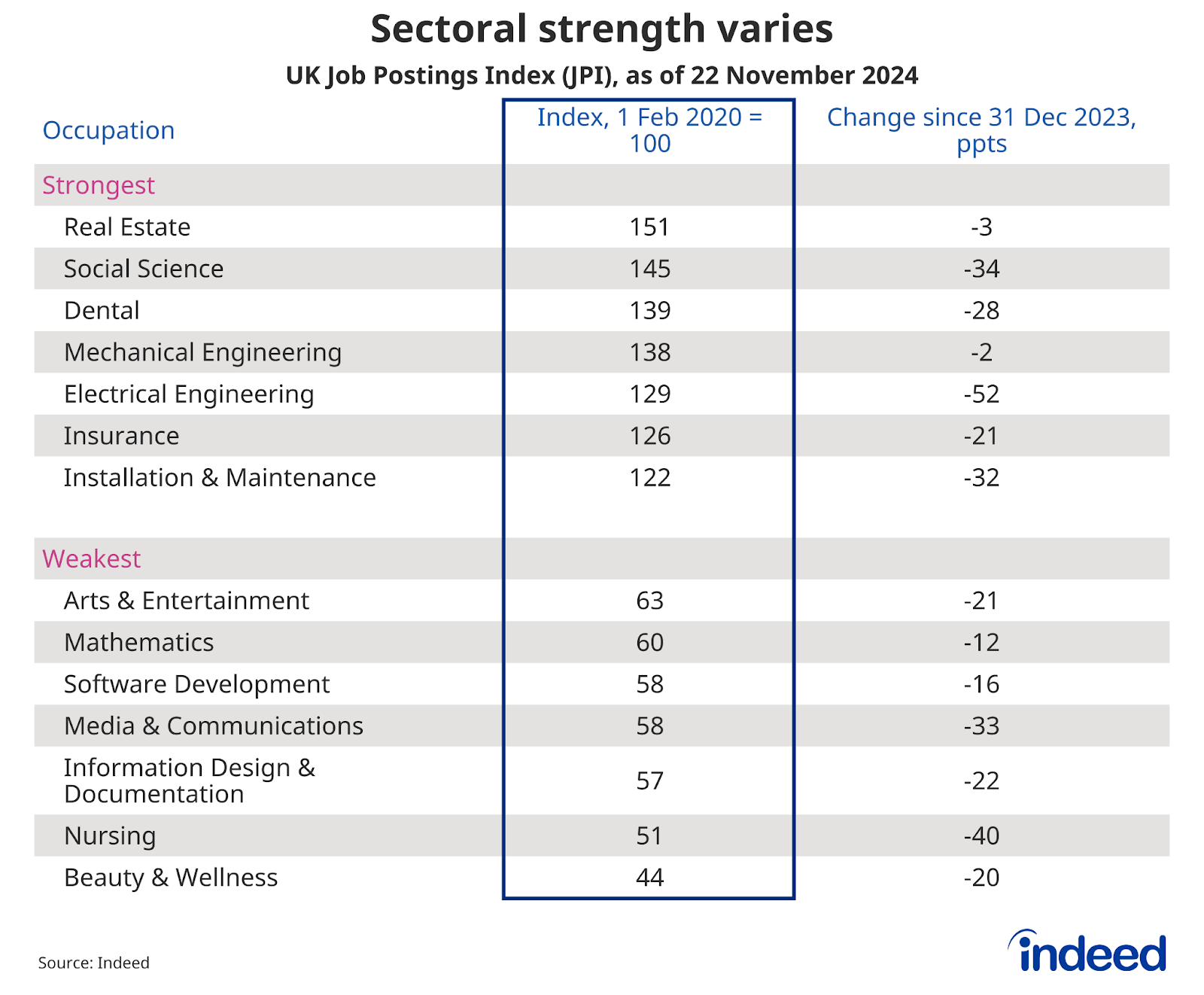

The slowdown has been broad-based across occupational categories — of the 48 sectors regularly tracked by Indeed, job postings were up over the past year in only one (the legal sector, +12 percentage points). The biggest falls were in the veterinary, electrical engineering, and security & public safety sectors.

Beauty & wellness and nursing postings stand furthest below the pre-pandemic baseline, followed by several tech-related categories. At the other end of the scale, real estate and social science are furthest above the baseline.

In 2025, certain categories could see a boost from the Labour government’s areas of policy focus. The construction and engineering sectors may get a boost amid a push to increase housebuilding and green energy, while certain public sector categories are likely to benefit from increased hiring in areas including education and healthcare.

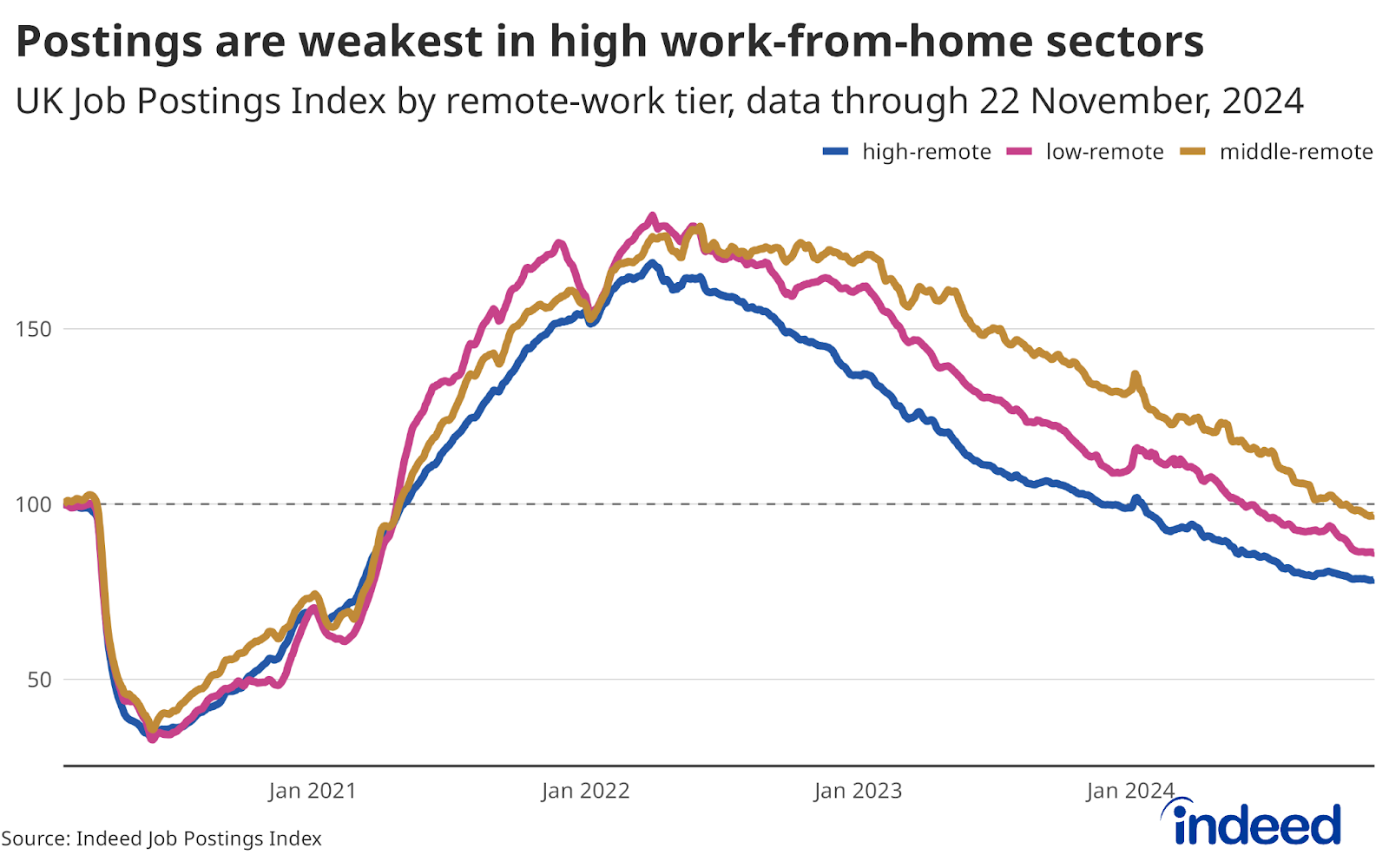

Job postings continue to trend weakest in categories that typically offer the most remote-work opportunities. Alongside the weakness in tech categories (which are the most likely to offer remote work), several professional categories are languishing among the weaker performers.

Reflecting their greater exposure to weakness in professional occupations, job postings in London and the South East (down 25.3% and 24.9%, respectively, from their pre-pandemic baselines) continue to underperform other regions. Northern Ireland (+21.4%), the North East (+18.6%) and Scotland (+7.7%) are the only regions where postings remain above pre-pandemic levels.

Zero-hours contracts have been gradually rising ahead of policy changes

A notable phenomenon in the UK labour market in recent years has been the growth of zero-hours contracts, in which set hours or pay are not guaranteed and employees do not have to accept any work the employer offers. Though they have attracted concern as a factor driving insecure work, proponents argue that their flexibility is beneficial for some workers. The Labour government’s Employment Rights Bill sets out changes around these contracts. Though initial plans for an outright ban were shelved, workers will now have the right to guaranteed hours should they want them.

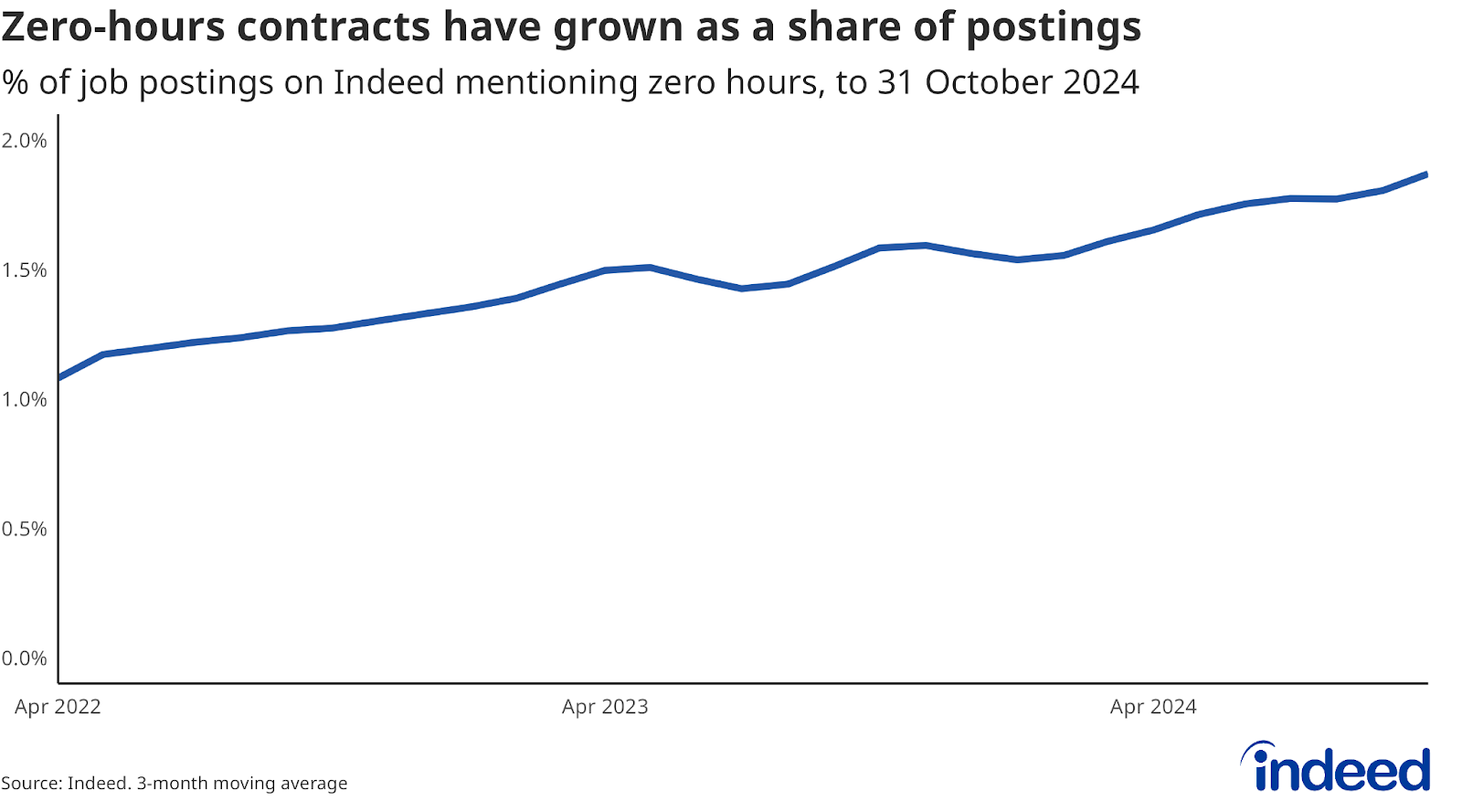

Despite government plans to restrict these contracts, they continue to rise in popularity in job postings. The share of job postings mentioning zero-hours arrangements stood at 1.9% in October, having gradually risen from around 1.1% back in April 2022. It will be interesting to see if this trend changes as a result of the legislation once implemented.

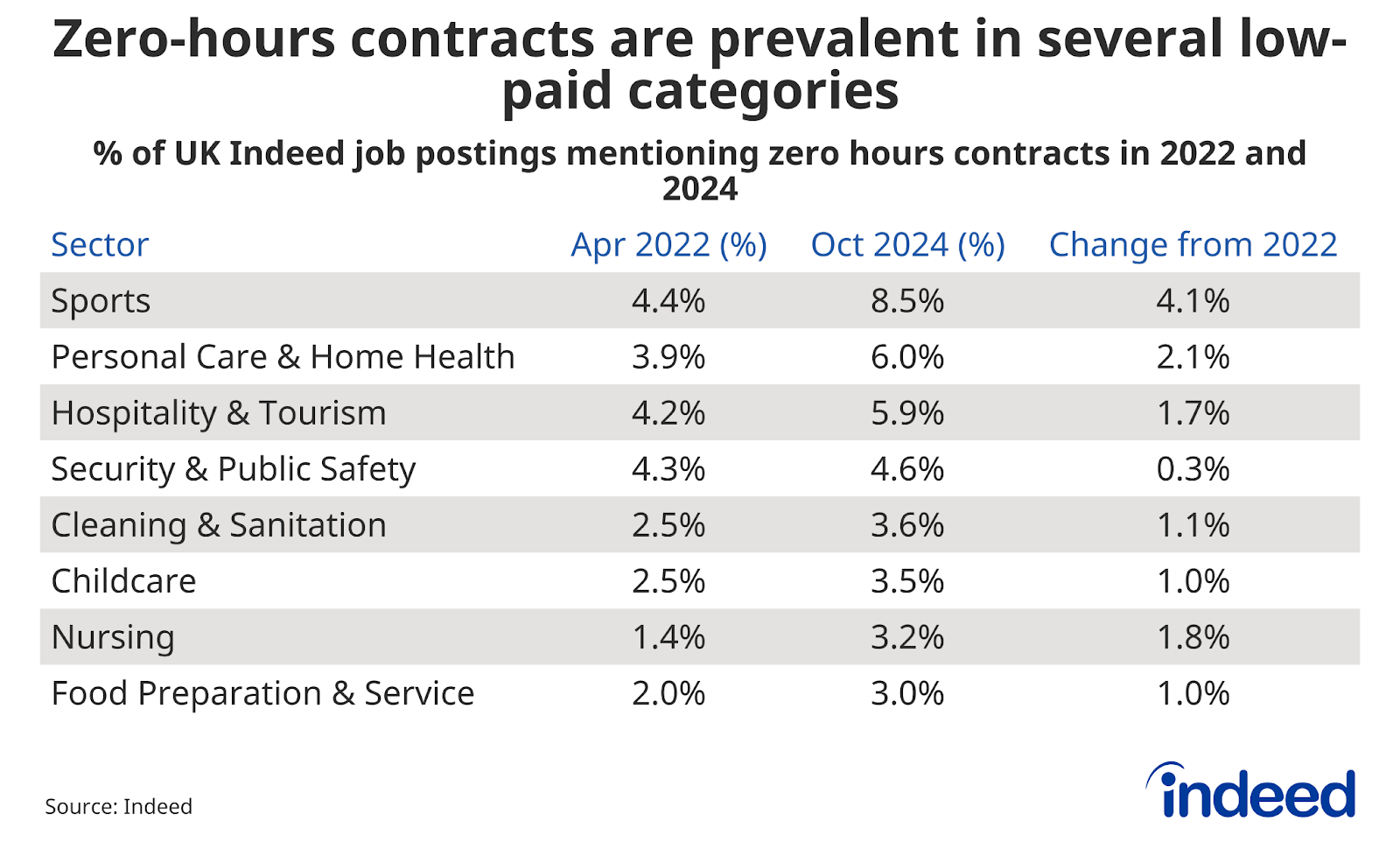

Zero-hours contracts are prevalent in job postings across a range of low-paid occupations, led by the sports category (8.5% of sports job postings mentioned a zero-hour contract in October), followed by personal care & home health (6.0%) and hospitality & tourism (5.9%).

Wage growth has persisted, but is likely to weaken

Wage growth has cooled from peaks but remains robust. ONS data shows regular pay rising at a 4.8% annual pace in the third quarter. With inflation well down from peaks and rising 2.9% over the same period, that means workers are seeing solid real-term annual pay growth of 1.9%. Pay has been rising in real terms since the middle of 2023, making up for the previous inflation-driven squeeze on purchasing power that characterised much of 2022. But the outlook for consumer spending is likely to remain muted, with households adopting a cautious attitude as higher taxes and the experience of repeated cost-of-living shocks prompt them to save rather than spend.

Given the overall softening in the labour market, wage growth is likely to cool further as the balance of power continues to shift in employers’ favour. Meanwhile, the increase in National Insurance contributions announced in the Budget presents a potentially significant headwind to wage growth after the new rules are adopted in April. The Office for Budget Responsibility (OBR) said it assumes that three-quarters of the increase will ultimately be funded by employers squeezing pay.

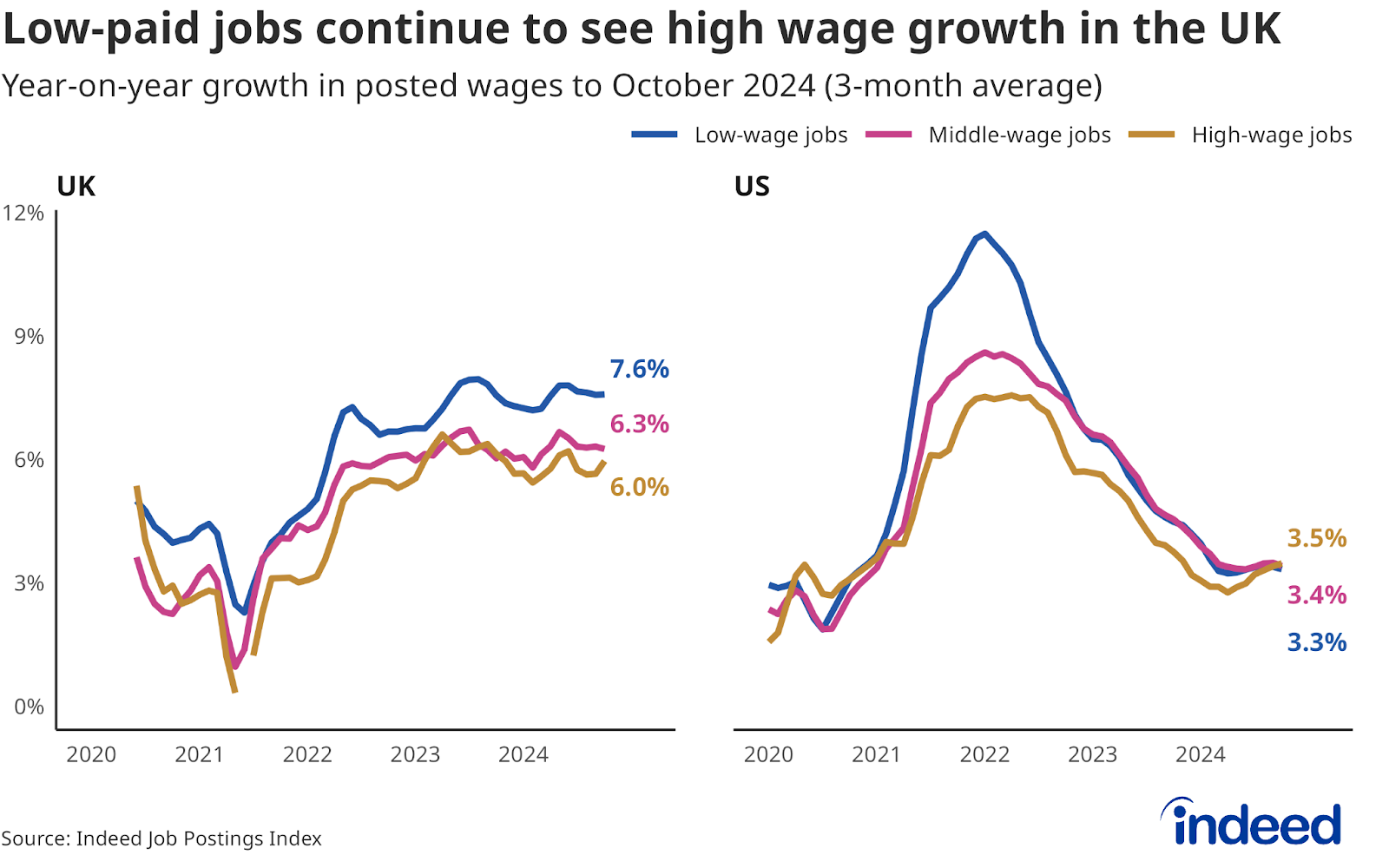

The Indeed Wage Tracker, which measures growth in posted wages in job listings, has dipped slightly from a recent peak of 7.0% year-on-year in June but continued to run at a high annual pace of 6.7% as of October. There remains a notable gap in posted wage growth between lower-paid occupations and higher-wage ones. Posted wages for the lowest-paying roles grew 7.6% year-on-year in October, versus 6.3% for mid-wage and 6.0% for high-wage jobs. Low-paid categories, including security, retail, customer service, cleaning and childcare, all saw annual posted wage growth of 8.0% or higher in October.

The gap in posted wage growth for low-paid occupations in the UK contrasts with the convergence seen in the US (as well as France and Germany). With the National Living Wage due to rise 6.7% in April (with even larger increases for younger workers as age bands are phased out), the divergence looks set to persist for some time yet.

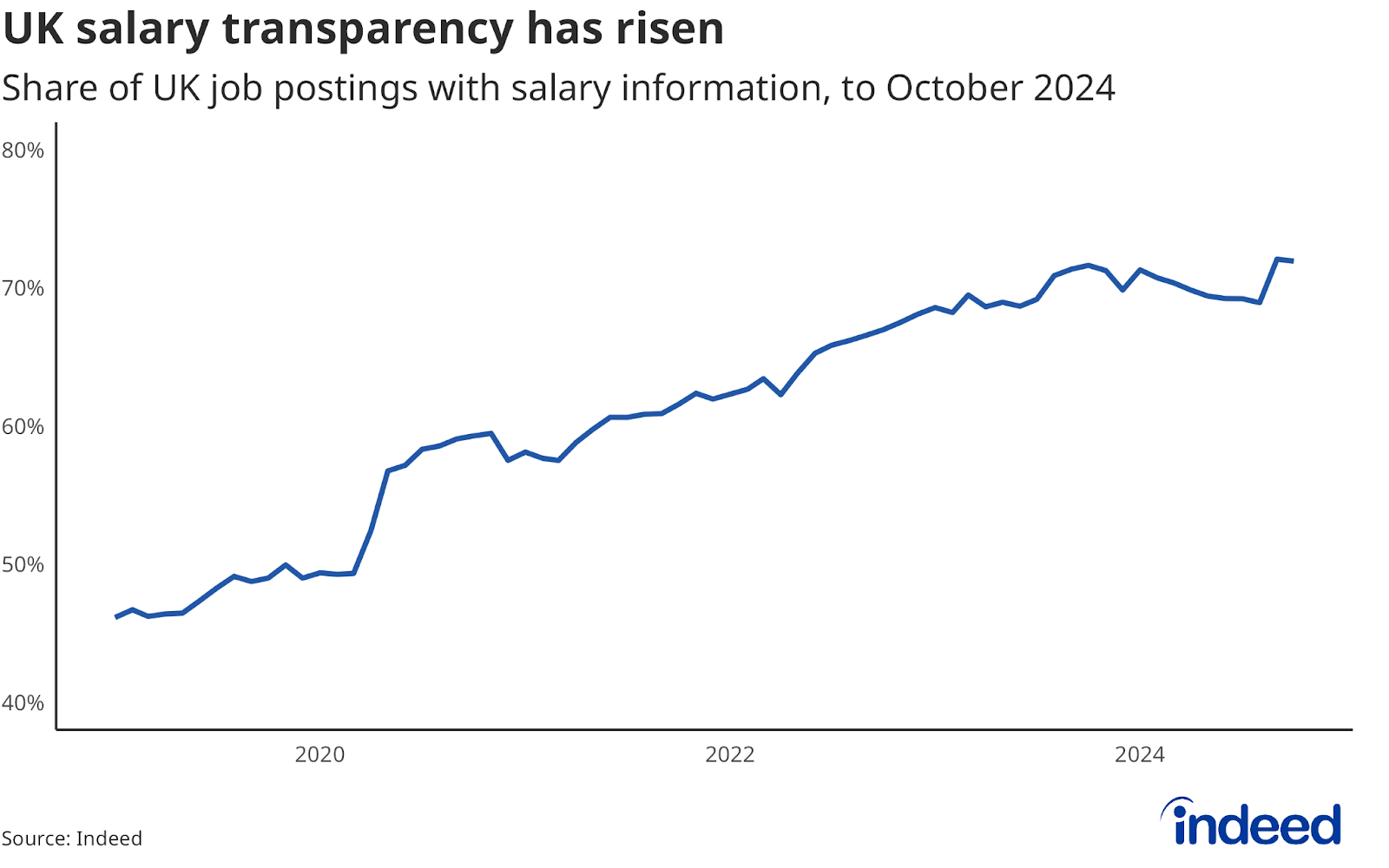

Pay transparency is rising

Though Brexit means the UK is outside the scope of upcoming EU pay transparency legislation, British employers have been increasingly moving towards greater pay transparency regardless. Salary transparency in UK job postings has been rising over the past five years, with 72% of postings including some pay information in October, up from less than 50% pre-pandemic. It seems clear that UK employers are mindful of the benefits of pay transparency, including attracting top talent and greater recruiting efficiencies gained by aligning salary expectations from the outset.

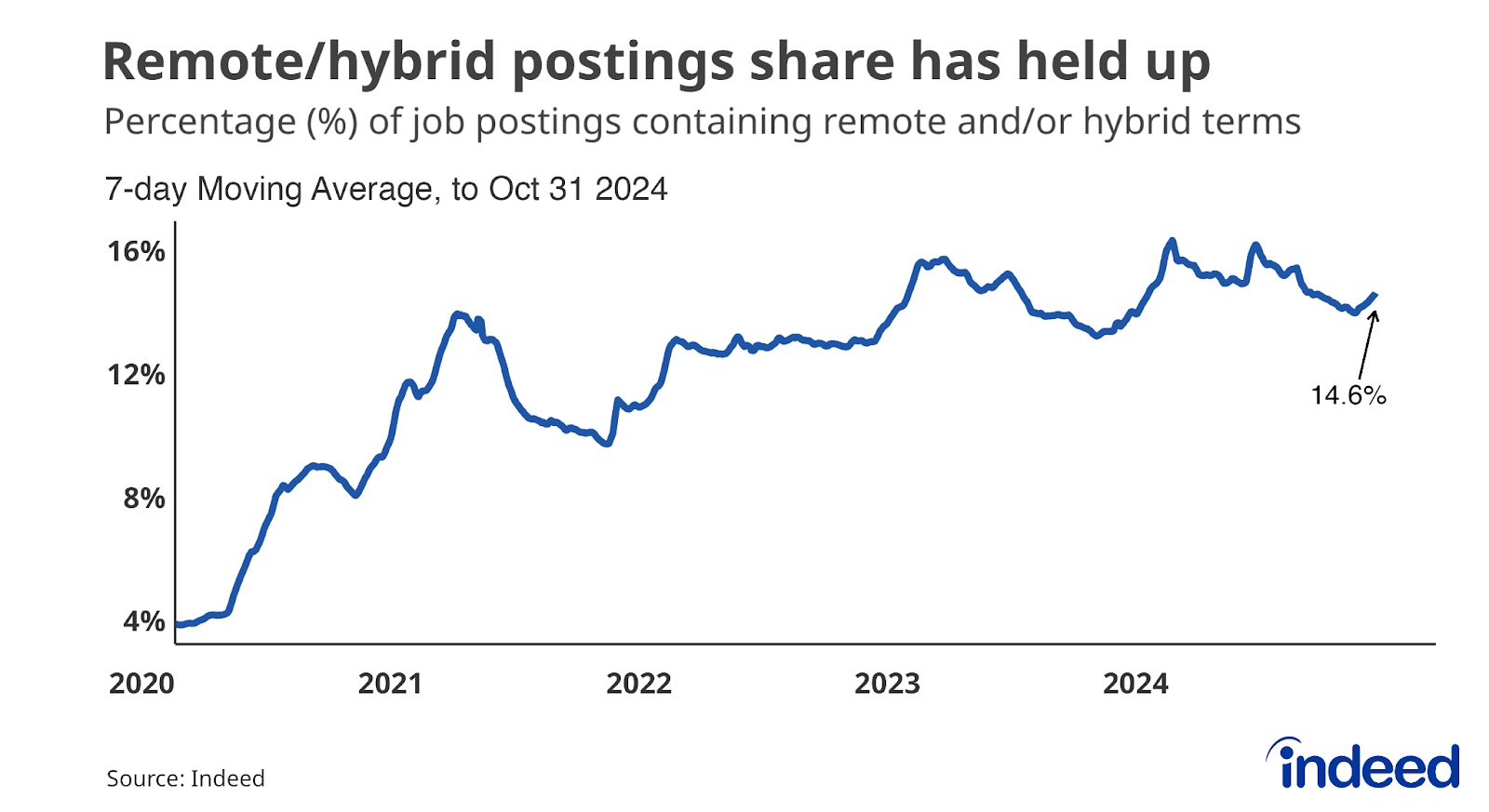

Remote and hybrid work persists despite RTO push

Despite all the attention on return-to-office (RTO), the share of UK job postings mentioning remote or hybrid work remains relatively high at 14.6%, down from a peak of 16.3% back in May, but well above the levels of around 3% seen pre-pandemic. While the average has been dragged down by weak job posting trends in tech categories — which tend to offer the most remote opportunities, in general — the remote/hybrid share remains close to peaks in several non-tech professional categories including accountancy, banking & finance, legal and marketing.

Jobseekers continue to search for remote and hybrid flexibility at similar rates to what we’ve seen since 2022, with these searches up around ninefold on pre-pandemic levels. While bosses at some high-profile companies are pushing hard on RTOs, offering location flexibility remains a powerful competitive edge for other employers. That’s particularly true for those businesses that might otherwise struggle to compete for top talent against larger competitors with a powerful employer brand. While the tug-of-war between employers and employees continues, location flexibility seems a trend that’s set to stay.

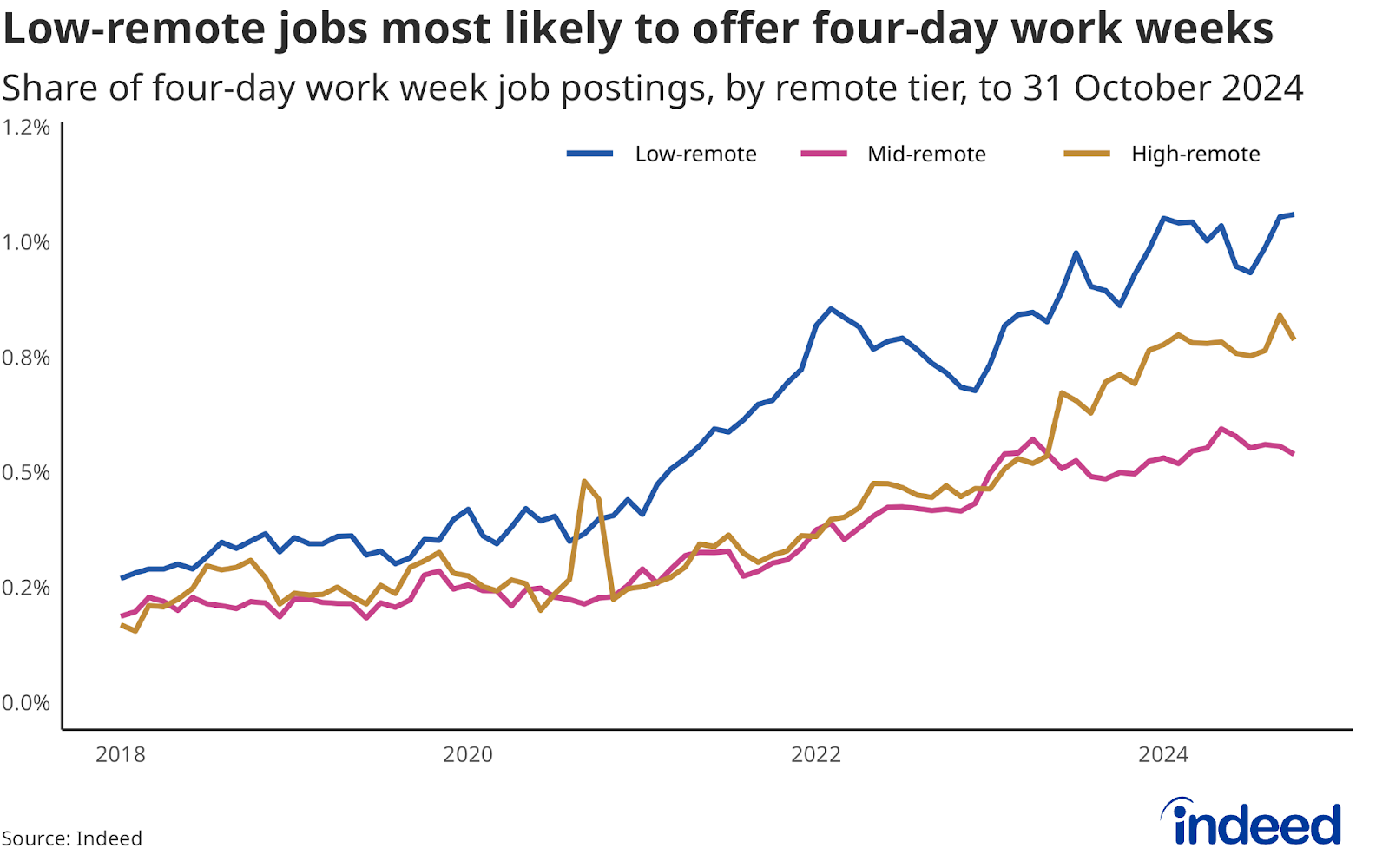

Of course, remote work isn’t feasible for all types of jobs. Employers for in-person occupations are offering other forms of flexibility, including four-day work weeks. The share of four-day-per-week postings is highest in the least remote-friendly occupations at 1.1%, versus 0.5% for mid-remote and 0.8% for high-remote. Veterinary (16.2%), childcare (4.0%) and education & instruction (2.5%) — roles that are among the most difficult to do remotely with any regularity — are the categories with the highest shares of four-day-week postings. Though still a niche phenomenon, four-day work weeks could continue to gain traction in 2025, with the first official pilot scheme underway.

High-remote categories which have recently seen growth in four-day weeks include software development, IT operations & helpdesk and mathematics.

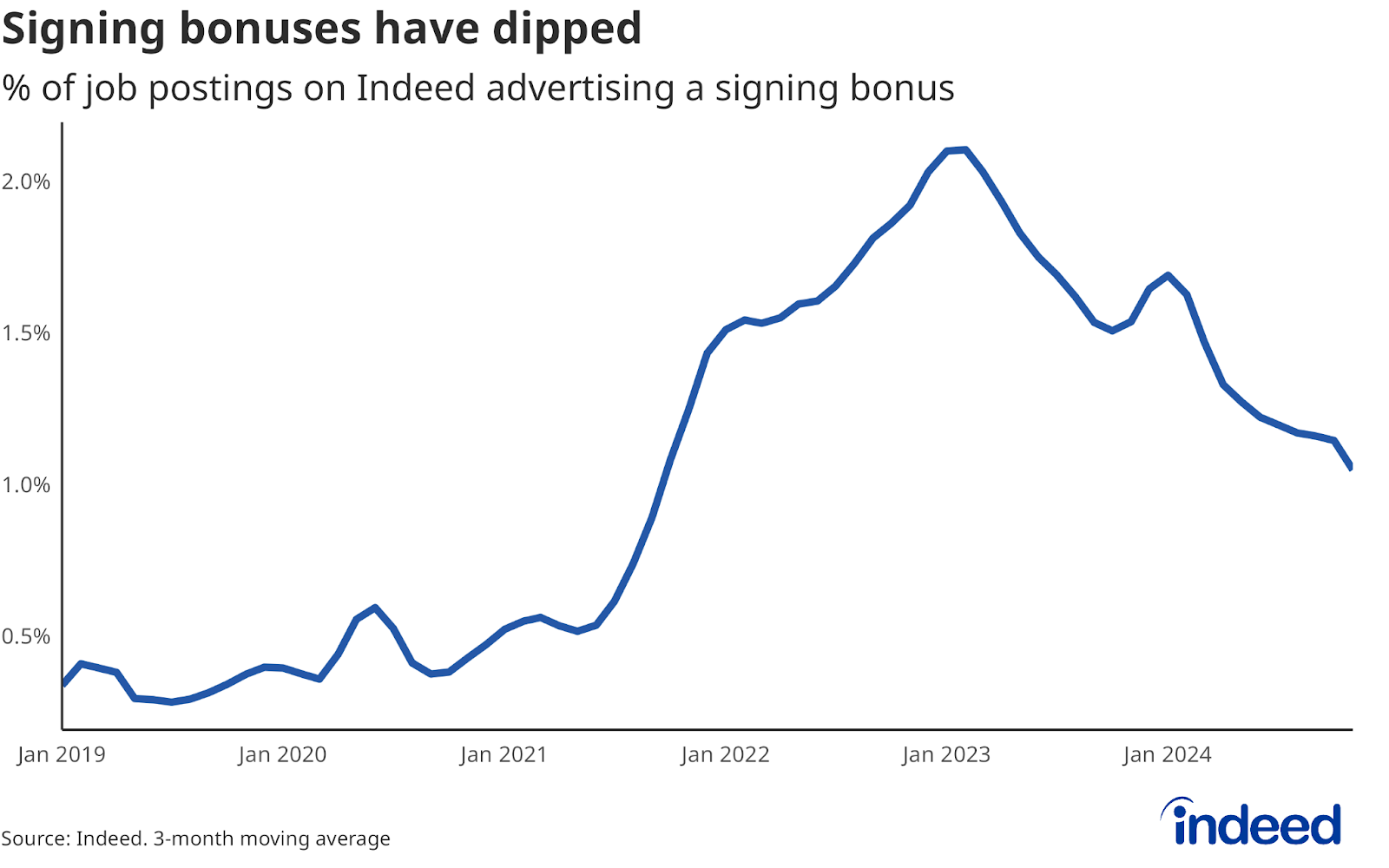

Signing bonuses have waned as the labour market cools

As the labour market has slowed, employers have been making less use of financial incentives such as signing bonuses (though they remain more prevalent than pre-pandemic). The share of job postings mentioning a signing bonus stood at 1.0% in November, down from a peak of 2.1% in February 2023. Signing bonuses are often an indication of where employers are experiencing pain points in finding suitable candidates for specific roles and/or locations and tend to fluctuate over time (for example we saw a spike for HGV drivers in 2021 when there were acute shortages). Veterinary, care and certain healthcare categories are currently most likely to offer a signing bonus. Though the continued cooling of the labour market suggests these incentives may continue to fade next year, they are likely to remain a feature in certain pockets of the market where recruitment difficulties persist.

Foreign labour offsets ageing UK population

The latest available statistics show that the UK population increased in the year to mid-2023 by the largest amount in 75 years. However, that was solely driven by record immigration, as UK deaths outnumbered births. In fact, the ‘natural population’ fell at the fastest rate in modern history. The situation of an ageing society reliant on immigration for population growth is expected to continue in coming years.

Immigration continues to play a vital part in supporting the UK labour market. That’s particularly true in sectors such as IT & communications, transport & storage and hospitality, where foreign workers are most prevalent. Post-Brexit immigration rule changes have resulted in a shift in emphasis to attracting immigrants from EU to non-EU countries.

The estimated number of foreign-born workers employed in the UK grew 1.0% in the last four quarters, while the number of UK-born workers fell 0.3%. While employers in higher-paying occupations are more likely to use visa sponsorship, some of those in lower-paying roles are advertising roles as open to workers who don’t speak English.

The UK has seen a rebound in foreign jobseeker interest after the pandemic, with almost 5% of clicks on UK jobs coming from outside the country. However, the relatively low proportion of clicks on postings in high-wage occupations in the UK contrasts with the stated aim of the current immigration policy to focus on attracting high-skilled foreign workers. That suggests Britain has more to do in the global competition to attract mobile, high-skill talent.

Demographic challenges are a particular concern for sectors, including construction, that have historically relied on foreign labour that is now less abundant post-Brexit. The Labour government plans an integrated approach to skills and training and the immigration system, but even if successful, it will take time for those plans to bear fruit for construction and other sectors grappling with skills shortages.

Employers will likely need to widen the net in future years to find the skilled workers they need. Faced with a similar challenge, some nations, including the US, have embraced skills-first hiring practices, including an openness to candidates without formal education degrees or a set amount of years’ experience in a given role. While education requirements aren’t commonly mentioned in UK job postings, we do see some evidence of increased skills-based hiring in certain high-skilled sectors, and expect these trends to continue into 2025 and beyond as skills shortages persist.

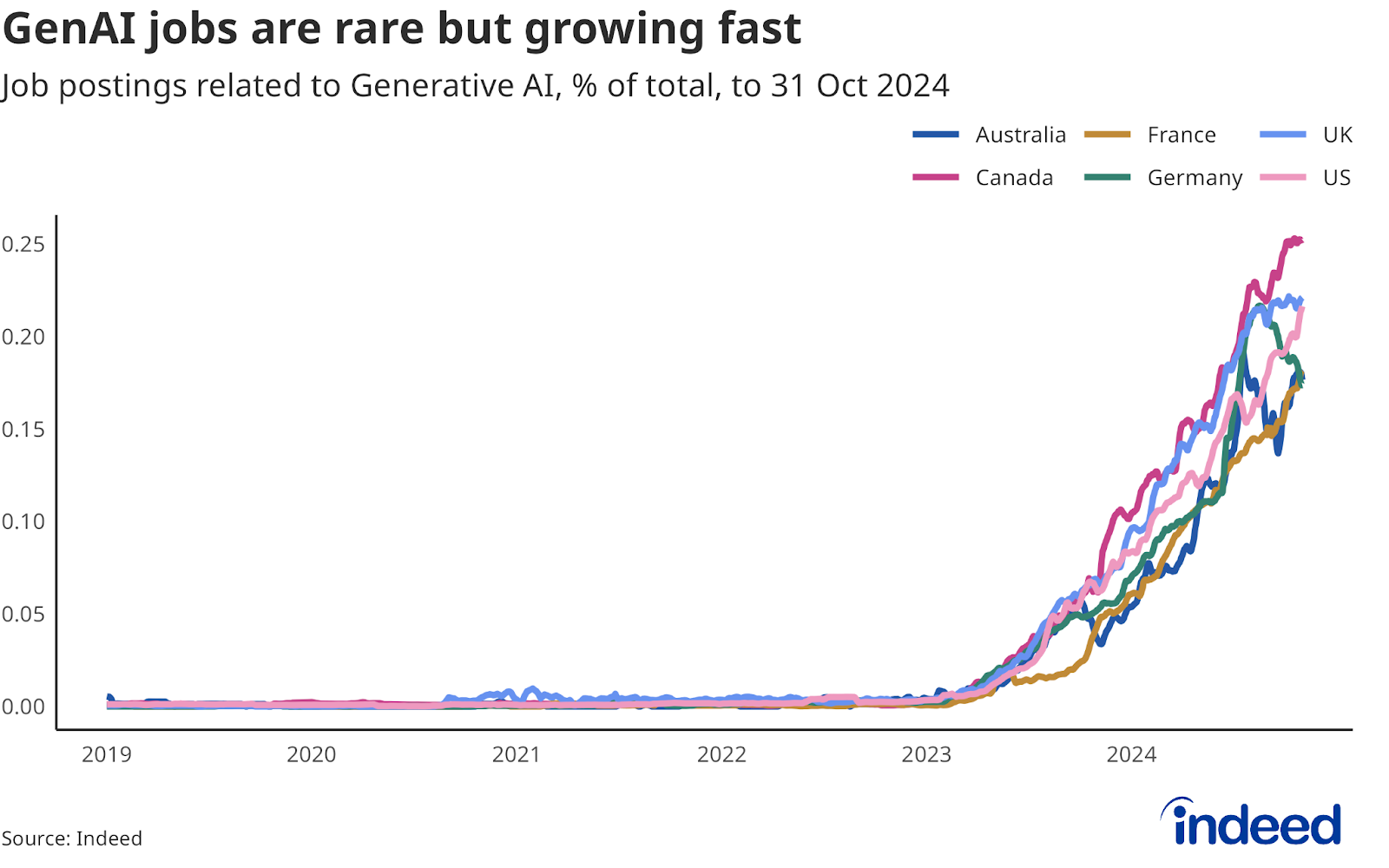

GenAI is creating new jobs, but is not yet widely adopted

While the full impact of artificial intelligence (AI) and particularly generative artificial intelligence (GenAI) on the labour market remains unknown, the tools are already making their mark. Despite bursting onto the scene just two years ago in late 2022, GenAI is already creating entirely new jobs, either for people building and maintaining the tools themselves, or for those using them widely in other occupations. Though still a very small share of overall UK job postings at 0.2%, the share of jobs mentioning one of several GenAI-related keywords has been rising rapidly from virtually zero prior to 2022. That growth will surely continue as organisations continue to develop and integrate the new technologies in their businesses.

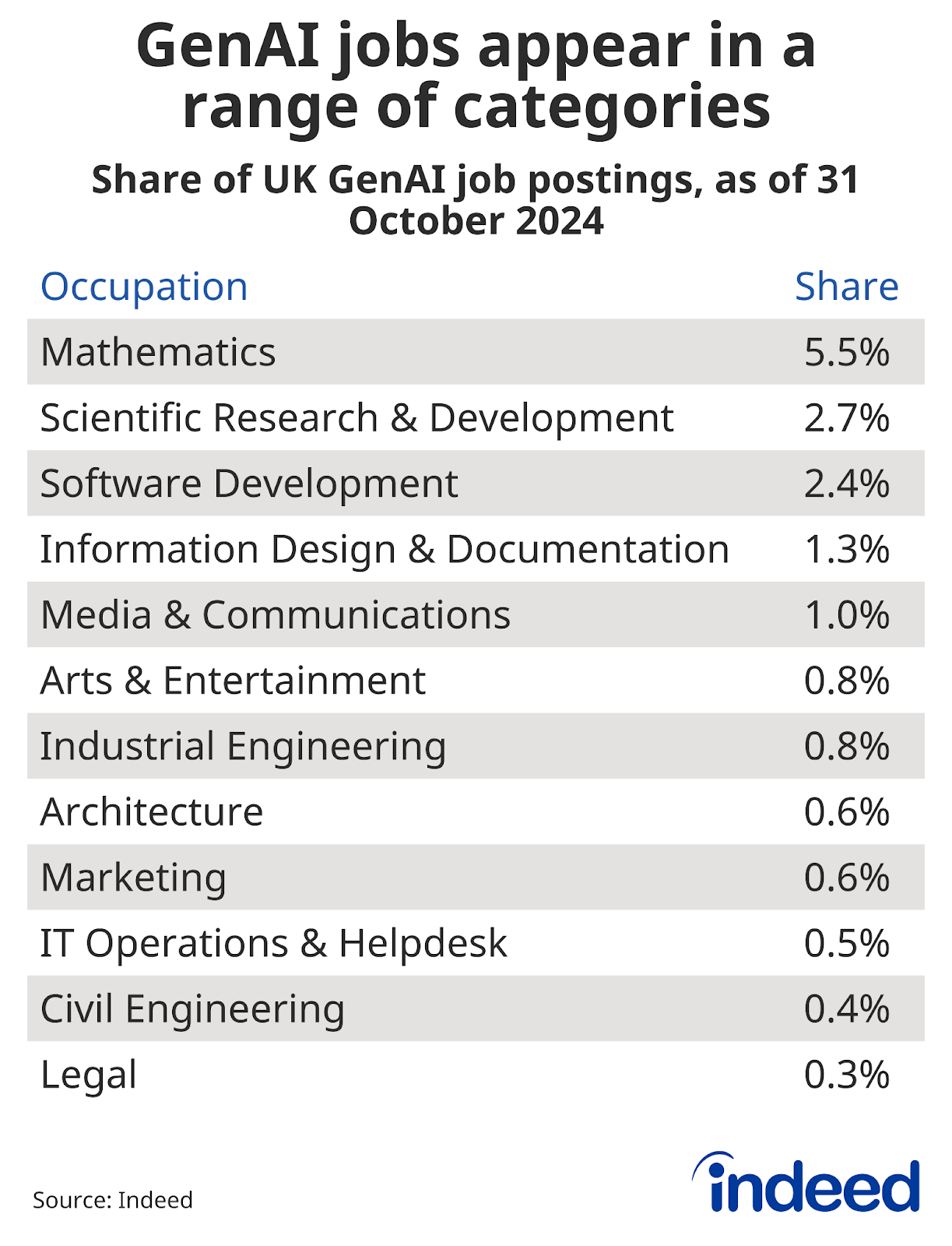

GenAI jobs are appearing across a range of occupational categories. The highest share of GenAI postings is found in the mathematics category (which includes jobs like data analysts, data scientists and statisticians), where 5.5% of all jobs are GenAI-related. Scientific research & development is in second place with 2.7%, followed by software development at 2.4%.

Based on our previous analysis of GenAI replacement risk, we find that certain UK occupational categories have been faster to adopt GenAI than expected. These include architecture, arts & entertainment, industrial engineering, IT operations & helpdesk and scientific research. Conversely, administrative support and medical information have fewer GenAI job postings than expected.

Conclusion

The UK economy has shown resilience in 2024, performing better than initially expected, but it faces challenges heading into 2025. Much will depend on the health of the labour market. It remains to be seen how employers react to the various policy changes. Even if warnings of mounting job losses don’t come to pass, job creation looks to be slower and the combination of slowing pay growth and higher taxes is likely to impact workers’ pay packets.

Policymakers’ jobs continue to be made harder by unreliable statistics, though there is consensus that despite having cooled, the labour market remains tight and measures to boost the supply of workers would be welcome. That would help ease the sticky wage inflation which continues to put pressure on businesses’ margins, constrain central bankers’ ability to cut interest rates and limit the growth of the UK economy.

Few sectors defied the hiring slowdown this year, but there are some pockets which held up better than others. While finding a job is likely to remain tough in some areas, particularly some types of knowledge work, there are other areas of the labour market which continue to offer a decent amount of opportunities for jobseekers, including certain engineering categories, installation & maintenance and certain healthcare occupations. For employers, remaining competitive on pay and benefits remains important to attracting the best talent.

That said, the balance of power has certainly swung towards employers as the labour market has softened, as evidenced by the fall in job postings, decline in signing bonuses, easing wage growth and rising zero-hours contract postings.